Original Author: PANews, Zen

July has come quietly, and most of this year has passed. Unlike last year when the market entered a bear market and continued to bottom out, and the industry was wailing, for practitioners in the cryptocurrency and Web3 industry, the first half of 2023 will be a period of rising, lively and doubtful coexistence. The market trend can sometimes boost confidence. At times it seemed hope was crushed. From the LSDFi narrative to the Shanghai upgrade, from the meme craze to the entry of Wall Street, amidst the twists and turns and shocks, Bitcoin finally temporarily stabilized above $30,000 in the middle of the year.

In the past half a year, the AI sector has had the same scenery in the field of science and technology, just like the blockchain industry that received countless favors and huge investments one or two years ago. However, under the background of the “monkey market” where the development of this industry is still unclear and the market is jumping up and down, the primary blockchain market in the first half of the year is also difficult to stabilize, and the financing situation varies greatly from month to month. Great disparity.

According to PANews statistics, there were 689 investment and financing events in the first half of 2023, a year-on-year decrease of 18.9% and a quarter-on-quarter decrease of 14.7%; the total financing scale exceeded US$5.97 billion, a year-on-year decrease of 74.3% and a quarter-on-quarter decrease of 47.9%. Among the financing in the first half of the year, more than US$2.36 billion was invested in the infrastructure and tools track, accounting for 39.1%, and there were 209 financing events, accounting for 30.29%, the highest among all vertical fields.

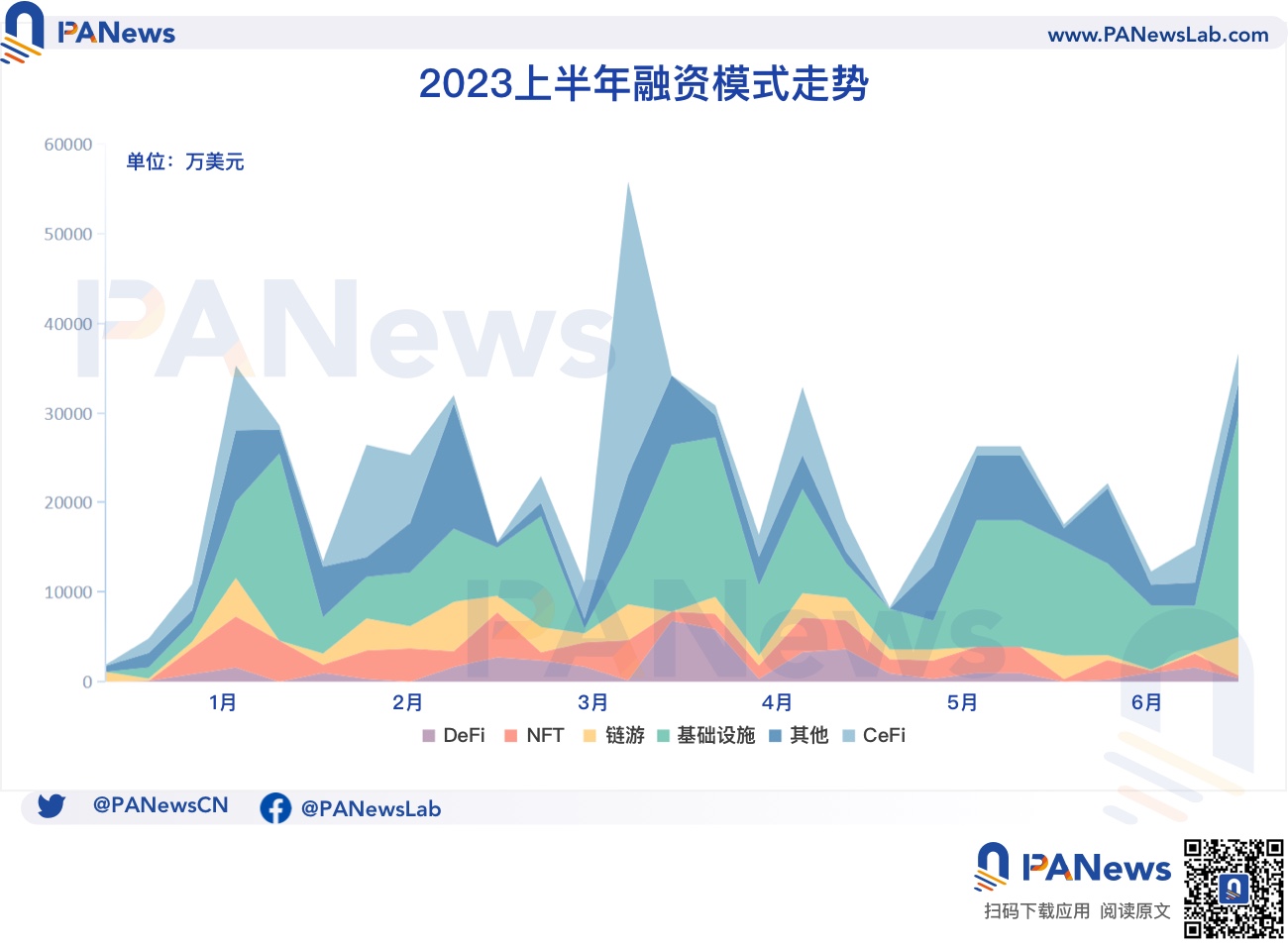

Financing overview in the first half of the year

In the first half of the year, the activity of the primary market was basically synchronized with the sentiment and heat of the secondary market, showing a strong positive correlation. At the beginning of the new year, the bear market in the encryption market has dropped to a freezing point. In the first two weeks of the year, there were no more than 10 investment and financing events announced in a single week, and the total financing scale was below 50 million US dollars. Then when the industry picked up, during the Maverick market trend from mid-to-late January to late April, the heat of the primary market ushered in a sharp rebound, and all tracks entered the best market in the first half of the year in April. According to the data of the PA column “Financing Weekly”, during this period, an average of 30 financing events were announced every week, and the average weekly financing scale exceeded 270 million US dollars.

It is worth mentioning that during the entire period of the Mavericks market, whenever the secondary market pulls back, the popularity of the primary market will drop sharply, but the reaction is slightly delayed. For example, in a correction in early March this year, the price of Bitcoin fell to around US$20,000 again, and then began to rise sharply from March 12. By March 20, the price of Bitcoin had rebounded to above US$28,000. , while the primary market in the same period was relatively bleak. According to the PA column “Financing Weekly”, from March 13th to 19th only 22 investment and financing events were announced, with a capital scale of 110 million US dollars, far below the weekly average level of the entire period.

The week with the largest number of investment and financing events announced in a single week in the first half of the year was from January 16 to January 22. During this week, 42 investment and financing events were announced, with a total financing scale of 350 million US dollars, including infrastructure, tools and blockchain/Web3 There were 22 cases in the application category; the largest single-week financing in the first half of the year was from March 20 to March 26, exceeding 558 million US dollars, and there were 26 investment and financing events. This week, the decentralized financial field ushered in an explosion. Over US$320 million in financing, of which eToro alone, a multi-asset investment platform, raised US$250 million at a valuation of US$3.5 billion. This financing is also the largest single financing event in the first half of this year.

The performance of each track is as follows:

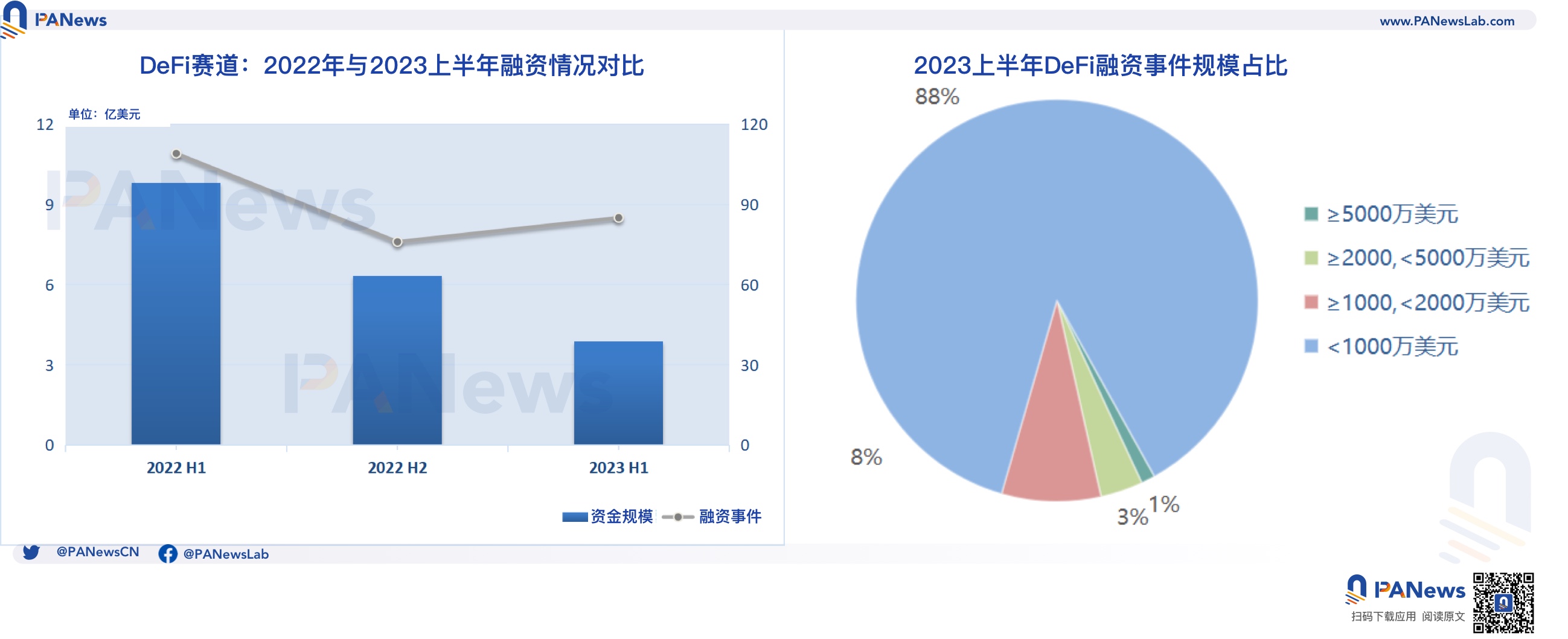

DeFi: The number of projects is not decreasing, and the large amount of financing is less

In the first half of the year, the financing scale of the DeFi track exceeded US$384 million, a year-on-year decrease of 60.5% and a month-on-month decrease of 38.8%; a total of 85 financing events were announced, a year-on-year decrease of 22% and a month-on-month increase of 11.8%. The financing scale of this track is mainly concentrated below 10 million US dollars, accounting for 88%, which is the highest in the track; there are only 4 projects with a financing amount of more than 20 million US dollars, accounting for about 4%. Among them, the project that received the largest financing was EigenLabs, the developer of the centralized financial (DeFi) platform EigenLayer, which raised $50 million in Series A financing led by Blockchain Capital. Other participating investors include Electric Capital, Polychain Capital, Coinbase Ventures and others.

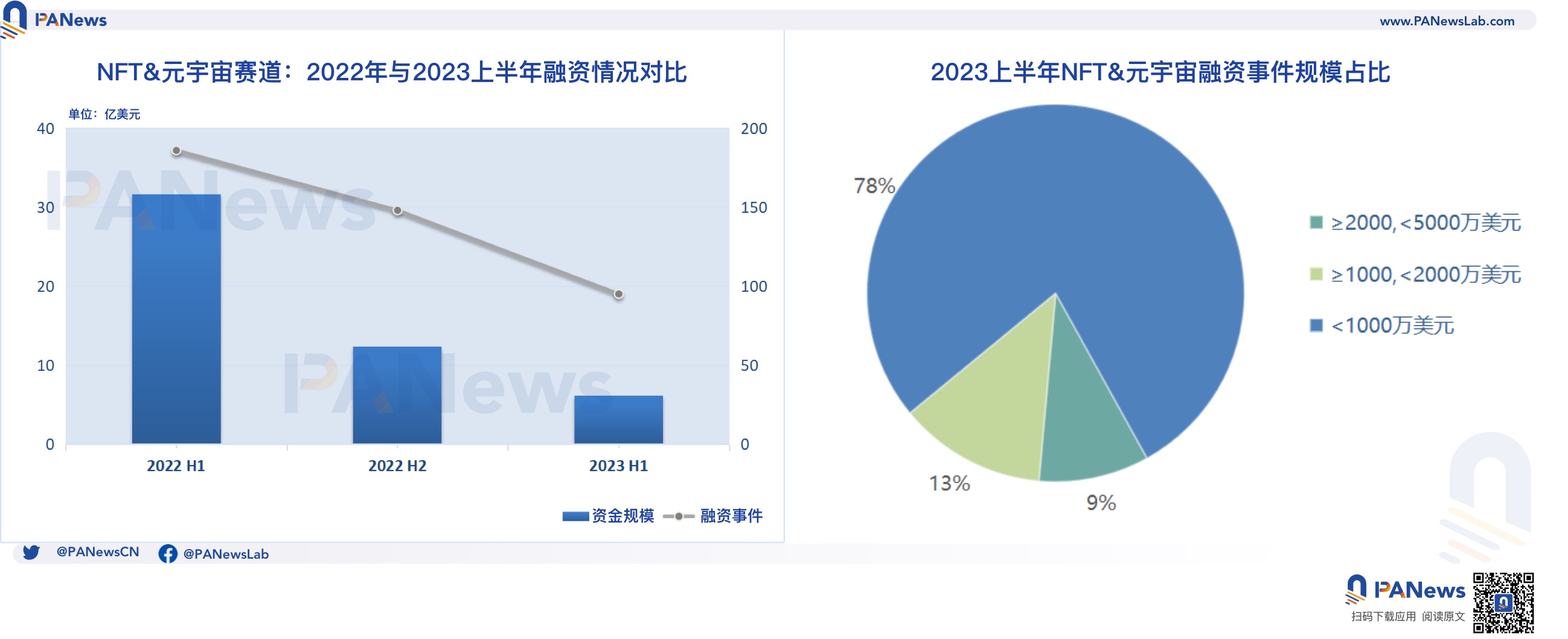

NFT&Metaverse: The track is deep, and the heat continues to decline

In the first half of the year, the financing scale of NFT and Metaverse track exceeded US$611 million, a year-on-year decrease of 80.6% and a month-on-month decrease of 50.4%; a total of 95 financing events were announced, a year-on-year decrease of 48.9% and a month-on-month decrease of 35.8%. On the whole, since last year, the track has shown a sharp decline in terms of both its scale and the number of projects. However, if we only look at the statistics in the first half of this year, the track showed steady growth from January to April, followed by a cliff-like decline, which is basically the same trend as other tracks. In the first half of this year, there were no projects that could raise more than 50 million yuan in NFT and metaverse track. There were 21 projects with a financing amount of 10 million to 50 million US dollars, accounting for about 22%.

According to statistics, among the 611 million US dollars raised by the track, more than 325 million US dollars flowed into the metaverse field, accounting for about 53%. Sandbox, SoftBank and Kingsway Capital led the round, with participation from HodlCo and Gemini Frontier Fund. The largest financing for NFT is the A1 round of financing of Candy Digital, a digital collection platform. According to SEC filing documents, it raised more than 38 million US dollars from 14 investors through equity issuance.

Chain games: capital diving, the market fell sharply

In the first half of the year, the financing scale of chain game tracks exceeded US$470 million, a year-on-year decrease of 74.7% and a month-on-month decrease of 70.3%; a total of 86 financing events were announced, a year-on-year decrease of 41.1% and a month-on-month decrease of 22.5%. Chain games and gamefi are the tracks that many people in the industry are optimistic about. Many investment research institutions report that they regard it as the main direction for the large-scale adoption of blockchain/Web3 technology. However, its market performance is not satisfactory. No matter the inflow of funds or the scale of financing, there is a big gap compared with last year, and the market has plummeted in the first half of this year.

Like the NFT and Metaverse track, in the first half of this year, no chain game project has received more than 50 million US dollars in financing. There are 18 projects with a financing amount of 10 million to 50 million US dollars, accounting for about 21% . Icelandic game developer and publisher CCP Games raised $40 million in the largest financing round, led by Andreessen Horowitz (A16z), with participation from Makers Fund, Bitkraft, Kingsway Capital, Nexon, Hashed, and others. The funds will be used to produce A triple-A blockchain game based on its flagship game Eve Online.

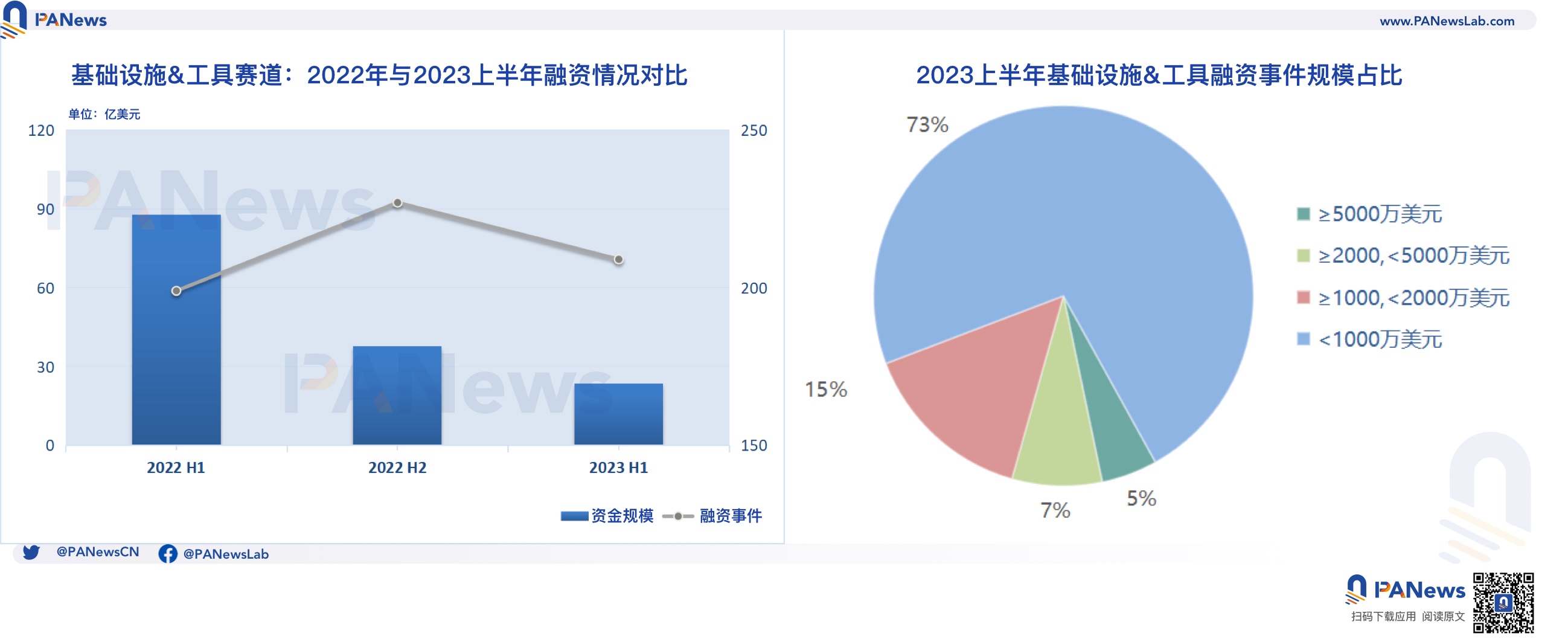

Infrastructure & Tools: Continue to lead in the long run

In the first half of the year, the financing scale of the infrastructure and tools track exceeded US$2.36 billion, a year-on-year decrease of 73% and a quarter-on-quarter decrease of 37.3%; a total of 209 financing events were announced, a year-on-year increase of 5% and a quarter-on-quarter decrease of 8%. The blockchain is still in its early stages, and infrastructure construction and tool innovation may remain the theme of the industry for a long time to come. As a long-term leading vertical field, in the first half of the year, there were 51 financing events with a scale of more than 10 million US dollars, accounting for about 27%; there were 10 projects with a financing amount of 50 million US dollars or more, accounting for about 5%.

Among them, the project that received the largest financing scale is Islamic Coin, an encryption project that complies with Shariah law. It received US$200 million in investment from digital asset investment company ABO Digital, which brought the total funding received by the project to US$400 million. In addition, LayerZero Labs, a cross-chain interoperability protocol, completed a US$120 million Series B round of financing at a valuation of US$3 billion, with participation from a16z Crypto, Christie’s auction house, Sequoia Capital, etc.; and Paris-based hardware wallet manufacturer Ledger in The majority of the $109 million financing goal was completed.

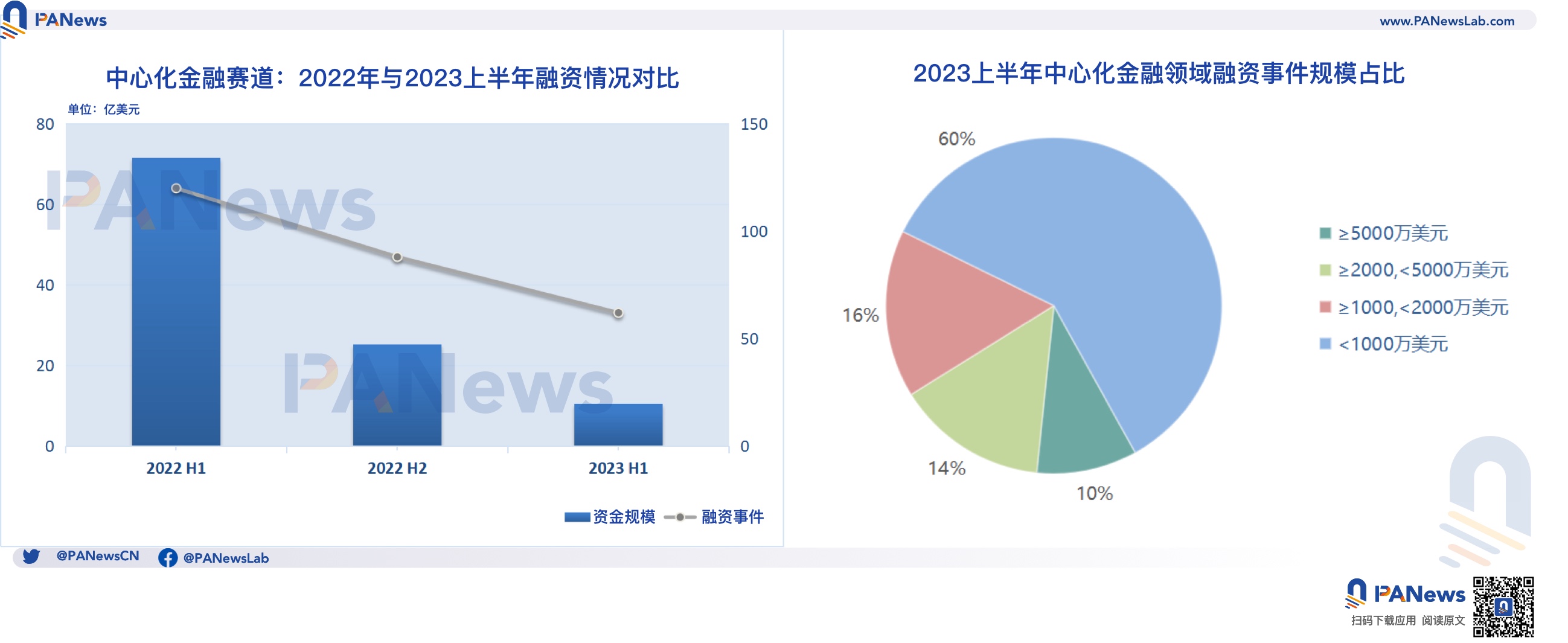

Centralized finance: the highest proportion of tens of millions of financing

In the first half of the year, the financing scale of other centralized finance exceeded US$1.04 billion, a year-on-year decrease of 20% and a quarter-on-quarter decrease of 36.4%. A total of 152 financing incidents were announced, a year-on-year decrease of 48% and a quarter-on-quarter decrease of 30%. Decentralized finance is still the field with the highest proportion of large-scale financing. There are 25 investment and financing events with a financing scale of US$10 million and above, accounting for nearly 40%, of which 6 are at a scale of US$50 million and above , accounting for nearly 10%.

In addition to eToro mentioned above, which raised US$250 million at a valuation of US$3.5 billion, other projects that have received large amounts of financing include: Salt, an encryption lender that was previously heavily influenced by FTX, completed a US$64.4 million Series A round of financing; And Taurus SA, a Swiss digital asset company, raised US$65 million through equity financing. Credit Suisse Group led the investment, and Deutsche Bank AG and Pictet Group participated in the investment.

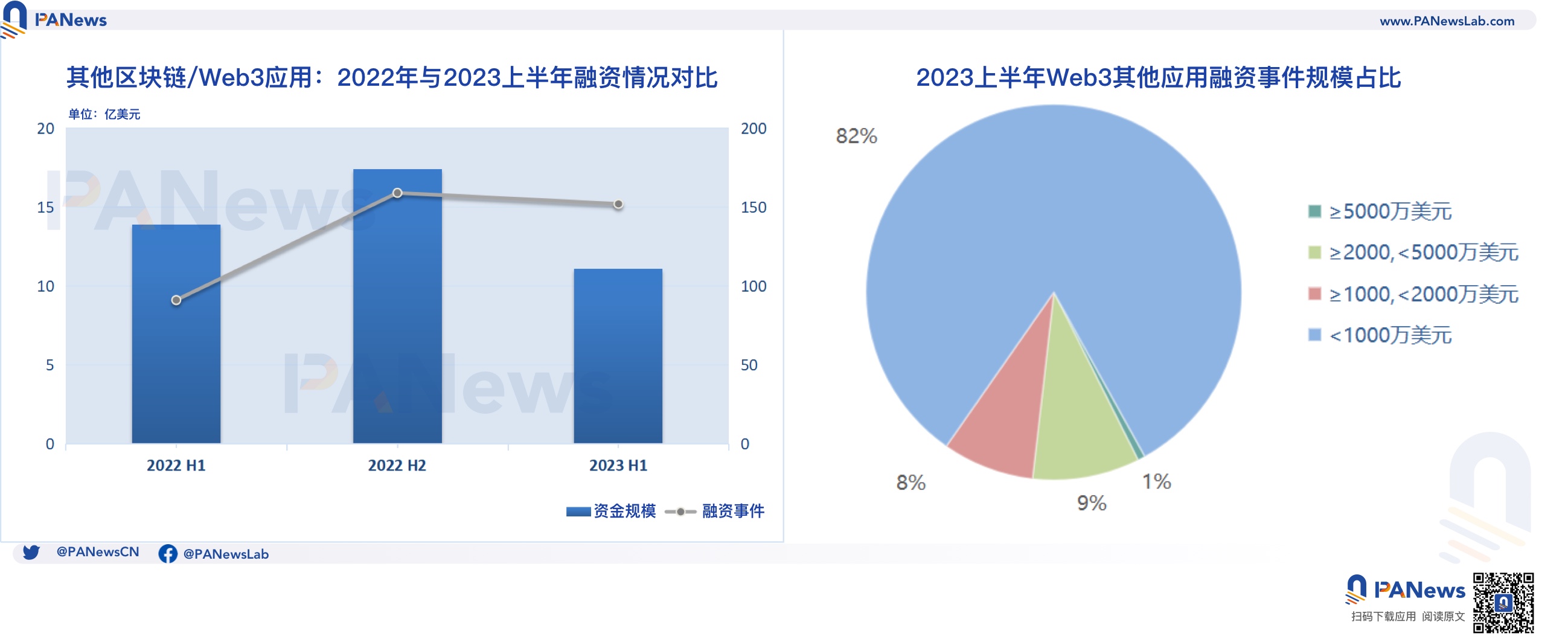

Others: least affected by the bear market, or due to the gradual landing of technology applications

This category mainly includes projects that combine DAO, media, market, social, education, mining, real estate, carbon neutral and other industries with blockchain and encryption technology. In the first half of the year, the total scale of financing in these application fields exceeded US$1.1 billion, a year-on-year decrease of 20% and a quarter-on-quarter decrease of 36.4%. A total of 152 financing events were announced, a year-on-year increase of 67% and a quarter-on-quarter decrease of 4.4%. Compared with last year, its financing projects only slightly decreased, and the decrease in financing amount was the lowest among the six fields.

The amount of financing obtained by projects in this category is generally relatively small, and there are 125 financing events with a scale of less than 10 million, accounting for 82%. Chain Reaction, a Tel Aviv-based blockchain chip startup, has raised $70 million, the track’s largest funding round, led by venture capital firm Morgan Creek Digital.