Author: Tristero Research

Compiled by: Felix, PANews

The slowest assets in the financial sector—loans, real estate, and commodities—are being bundled into the fastest market ever. Tokenization promises liquidity, but what it truly creates is merely an illusion: a highly liquid shell wrapped around an illiquid core. This mismatch is the RWA liquidity paradox.

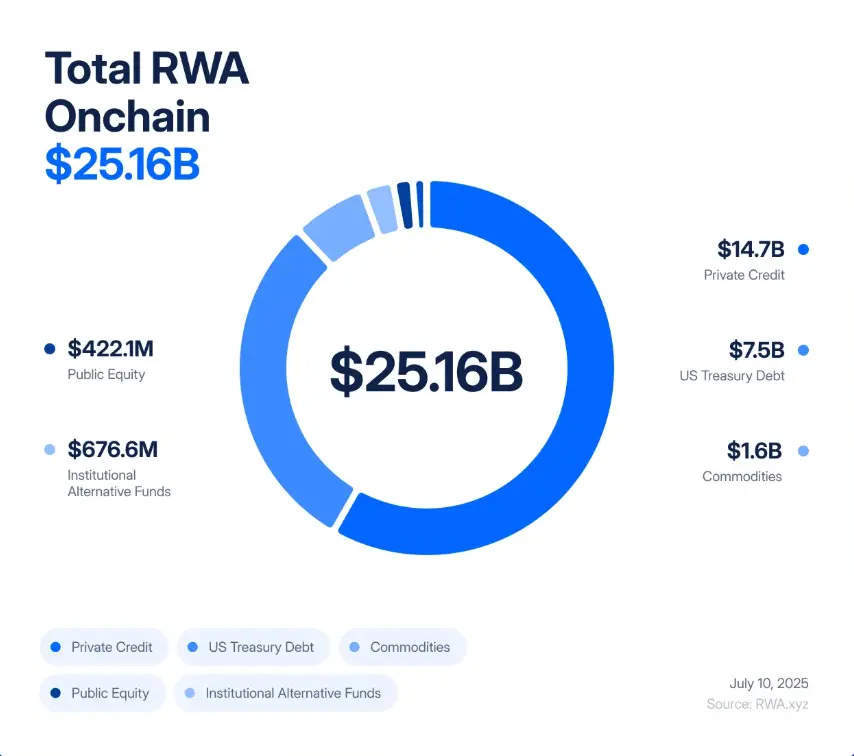

In just five years, tokenized RWA has evolved from an $85 million experiment to a $25 billion market, growing 245 times between 2020 and 2025, driven by institutional demand for yield, transparency, and balance sheet efficiency.

BlackRock has issued tokenized government bonds, Figure Technologies has placed billions of dollars in private credit on-chain, and real estate transactions from New Jersey to Dubai are being fractionalized and traded on DEX.

Analysts expect that trillions of dollars in assets will follow soon. To many, this seems like the long-awaited bridge between TradFi and DeFi — finally an opportunity to combine the safety of real-world returns with the speed and transparency of blockchain.

However, there are structural flaws beneath this enthusiasm. Tokenization does not change the fundamental nature of office buildings, private loans, or gold bars. These are all assets with poor liquidity and slow monetization—bound by contracts, registration agencies, and courts on both legal and operational levels. What tokenization does is wrap them in a highly liquid shell, allowing them to be traded, leveraged, and settled instantly. The result is that the credit and valuation risks that slowly transfer within a financial system are transformed into high-frequency volatility risks, whose contagion spreads not over months, but within minutes.

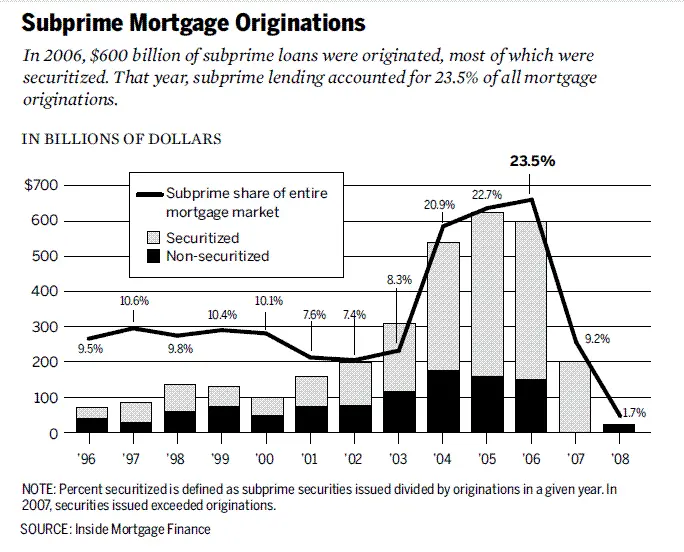

If this sounds familiar, it's because it has happened before. In 2008, Wall Street learned a painful lesson about the consequences of turning illiquid assets into “liquid” derivatives. Subprime mortgages slowly collapsed; collateralized debt obligations (CDOs) and credit default swaps (CDS) rapidly fell apart. The mismatch between real-world defaults and financial engineering triggered a global system failure. The danger today is that we are currently rebuilding this architecture—only this time it operates on the blockchain, and the crisis will spread at the speed of code.

Imagine a commercial property token in Bergen County, New Jersey. On the surface, the building appears solid: tenants pay rent on time, mortgage payments are made on schedule, and the title is clear. However, completing the legal procedures for the transfer of ownership—title verification, signatures, and submitting documents to the county—can take weeks. This is how the real estate industry operates: slowly, methodically, constrained by paper documents and the courts.

Now put this property on the blockchain. The ownership is held in a special purpose company that issues digital tokens representing partial ownership. Suddenly, once dormant assets can be traded around the clock. In an afternoon, these tokens may change hands hundreds of times on a DEX, be used as collateral for stablecoins in lending protocols, or be packaged into structured products promising “safe, real returns.”

There is a key point here: the building itself does not change at all. If the main tenant defaults, if property values decline, or if the legal claims of a Special Purpose Vehicle (SPV) are questioned, the real-world impact will gradually manifest over months or years. But on the blockchain, confidence can vanish in an instant. A rumor on X, a delay in oracle updates, or a sudden sell-off can trigger a chain reaction of automatic liquidations. The building does not move, but its tokenized representation may collapse within minutes—along with dragging down the collateral pool, lending protocols, stablecoins, and so on.

This is the essence of the RWA liquidity paradox: bundling illiquid assets in a highly liquid market creates an illusion that it makes the assets safer, but in reality, it makes them more explosive.

2008 slow motion vs. 2025 real-time footage

In the early 21st century, Wall Street transformed subprime mortgages (loans with poor liquidity and high risk) into complex securities.

Mortgages are pooled into mortgage-backed securities (MBS), which are then sliced into different tranches of collateralized debt obligations (CDO). To hedge risks, banks layered in credit default swaps (CDS). In theory, this alchemy transforms fragile subprime loans into “safe” AAA-rated assets. But in reality, it built a leveraged and opaque “tower” on an unstable foundation.

When the slow-spreading mortgage defaults collided with the rapidly developing CDO and CDS markets, the crisis erupted. Foreclosures on homes take months, but the associated derivatives can be repriced in seconds. This mismatch was not the only reason for the collapse, but it amplified localized defaults into a global shock.

RWA tokenization has the potential to repeat such mismatches, and at a faster pace. However, instead of layering subprime mortgages, it is about breaking down private credit, real estate, and government bonds into on-chain tokens. Additionally, we won't see credit default swaps (CDS), but rather “RWA enhanced” derivatives: options, synthetic products, and structured products based on RWA tokens. Furthermore, it is not about having rating agencies rate junk bonds as AAA, but about outsourcing valuations to oracle and custodians — the new trust black box.

This analogy is not superficial. The logical essence is the same: wrapping illiquid and slow-to-monetize assets in a structure that appears to be highly liquid; then allowing them to circulate in a market that moves several orders of magnitude faster than the underlying assets. In 2008, the entire system collapsed within months. In the DeFi space, a crisis can spread in just a few minutes.

Scenario 1: Credit Default Chain Reaction

A private credit agreement will tokenize $5 billion in small and medium-sized enterprise loans. On paper, the yield stabilizes between 8% and 12%. Investors view this token as safe collateral for borrowing and lending on Aave and Compound.

Subsequently, the real economy began to deteriorate. The default rate rose. The true value of the loan book declined, but the oracles relying on on-chain prices are only updated once a month. On the chain, the tokens still appear to be robust.

Rumors are rampant: some large borrowers have defaulted on their loans. Traders are scrambling to sell off before the oracle updates. The market price of the token has fallen below its “official” value, breaking the peg mechanism.

This is enough to trigger the liquidation bot. DeFi lending protocols record the price drop and automatically liquidate loans collateralized by that token. The liquidation bot repays the debt, seizes the collateral, and sells it on the exchange—further driving down the price. More liquidations follow. Within minutes, the feedback loop transforms a slow credit problem into a full-blown on-chain collapse.

Scenario 2: Real Estate Flash Crash

A custodian institution responsible for managing $2 billion worth of tokenized commercial real estate has been attacked by hackers, admitting that its legal rights to the properties may be compromised. Meanwhile, a hurricane has struck the city where many of these commercial properties are located.

The off-chain value of these assets is in question; the on-chain tokens immediately crash.

In the DEX, panicked holders rushed out. The liquidity of the automated market makers was drained. Token prices plummeted.

In the entire DeFi space, this token was once used as collateral. The liquidation mechanism was triggered, but the seized collateral was worthless and had extremely poor liquidity. The lending protocol left behind irretrievable bad debts. What was originally marketed as “institutional-grade on-chain real estate” instantaneously became a hole on the balance sheet of DeFi protocols — all TradFi funds related to it were also not spared.

Both situations demonstrate the same dynamic: the collapse of the liquidity shell is much faster than the response of the underlying assets. The building still stands, the loans still exist, but on-chain, their representative forms vanish without a trace in just a few minutes, dragging the entire system down.

Next Phase: Enhanced RWA

Finance never stops at the first layer. Once an asset class emerges, Wall Street (and now DeFi) builds derivatives on top of it. Subprime mortgages gave rise to mortgage-backed securities (MBS), followed by collateralized debt obligations (CDO), and then credit default swaps (CDS). Each layer promises to manage risk better; each layer also amplifies vulnerability.

RWA tokenization will not be an exception. The first wave is simple: the segmentation of credit, government bonds, and real estate. The second wave is inevitable: an enhanced version of RWA. Tokens are packaged into indices, divided into “safe” and “risky” parts, with synthetic products enabling traders to bet on or short a basket of tokenized loans or properties. Tokens backed by real estate in New Jersey and SME loans in Singapore can be repackaged into a single “yield product” and leveraged in DeFi.

Ironically, on-chain derivatives seem to be safer than the credit default swaps (CDS) of 2008, as they are fully collateralized and transparent. But the risks do not disappear—they mutate. Smart contract vulnerabilities replace counterparty defaults. Oracle errors replace rating fraud. Governance failures replace AIG. The result is the same: layered leverage, hidden correlations, and a system vulnerable to single points of failure.

Diversification commitment—a mix of government bonds, credit, and real estate in a tokenized basket—overlooks a reality: all these assets now share a common correlation vector: the DeFi infrastructure itself. If major oracles, stablecoins, or lending protocols fail, then regardless of how diversified the underlying assets are, all RWA-based derivatives will collapse.

The enhanced version of RWA products will be marketed as a bridge to maturity, proving that DeFi can reshape complex TradFi. However, they could also act as a catalyst, ensuring that when the first shock arrives, the system does not buffer but instead crashes.

Conclusion

The prosperity of RWA is touted as a bridge connecting TradFi and DeFi. Tokenization has indeed brought efficiency, composability, and new avenues for yield generation. However, it has not changed the nature of the assets themselves: even though the digital packaging of loans, houses, and commodities trades at blockchain speed, they still circulate slowly and lack liquidity.

This is the liquidity paradox. Bundling illiquid assets into a highly liquid market increases vulnerability and reflexivity. Tools that make the market faster and more transparent also make it more susceptible to sudden shocks.

In 2008, the subprime loan defaults took months to evolve into a global crisis. With tokenized RWAs, similar mismatches could spread within minutes. This does not mean abandoning tokenization, but rather designing with its risks in mind: using more conservative oracles, stricter collateral standards, and more robust circuit breakers.

It is not destined to repeat the mistakes of the last crisis, but if this paradox is ignored, it may ultimately accelerate the arrival of a crisis.

Related reading: Top university professors debate: Is Ethereum ready for RWA?