Futures

Access hundreds of perpetual contracts

TradFi

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

More

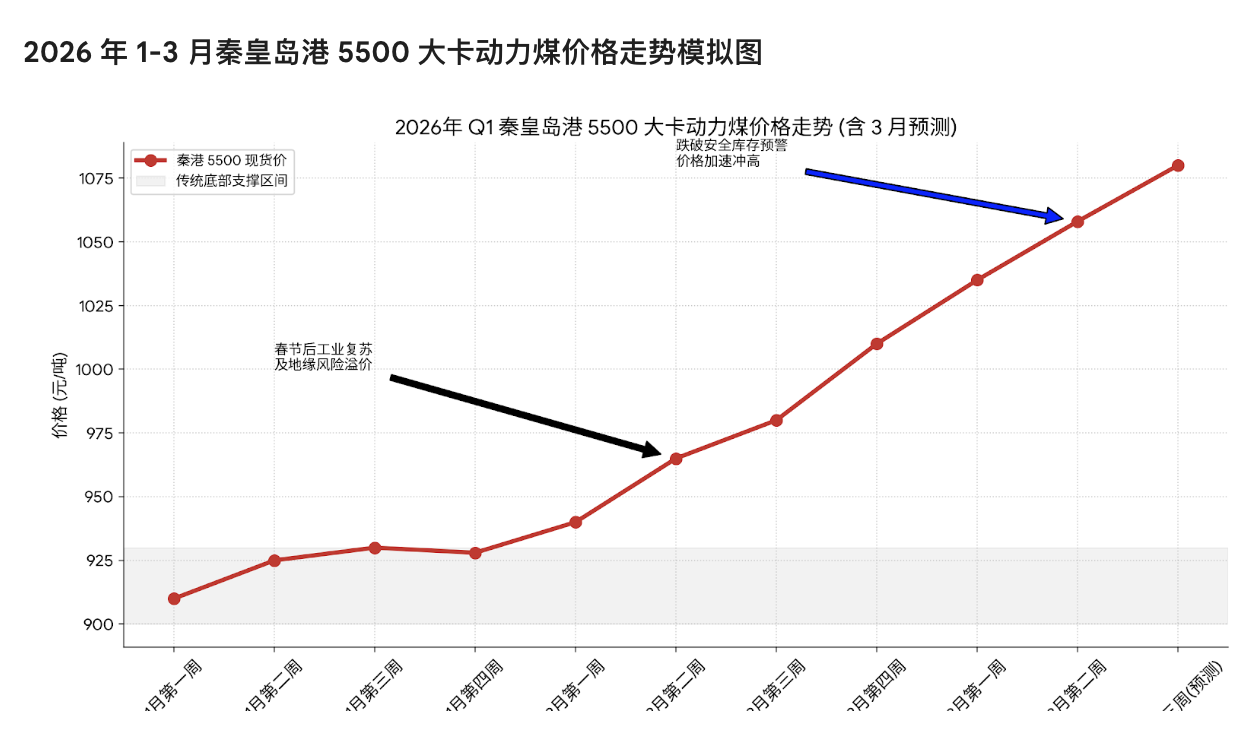

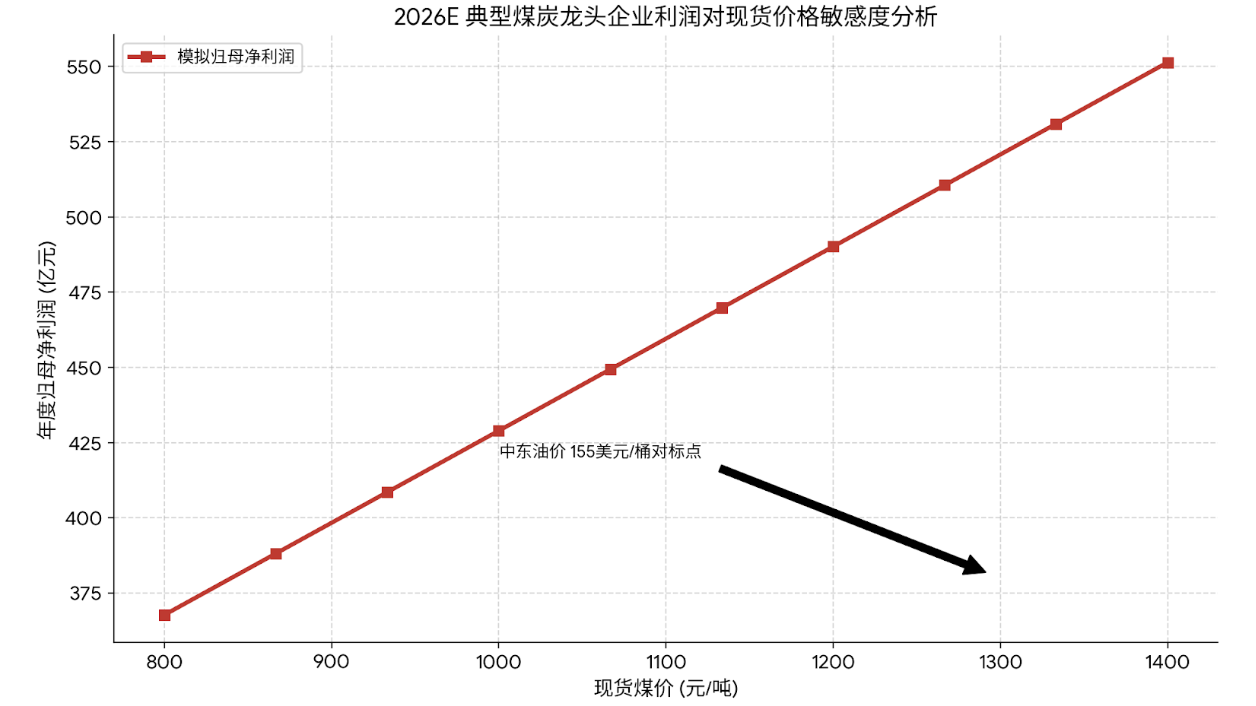

When oil prices surpass $150: coal may be entering a strategic reassessment window amid the global energy "dual-track split"

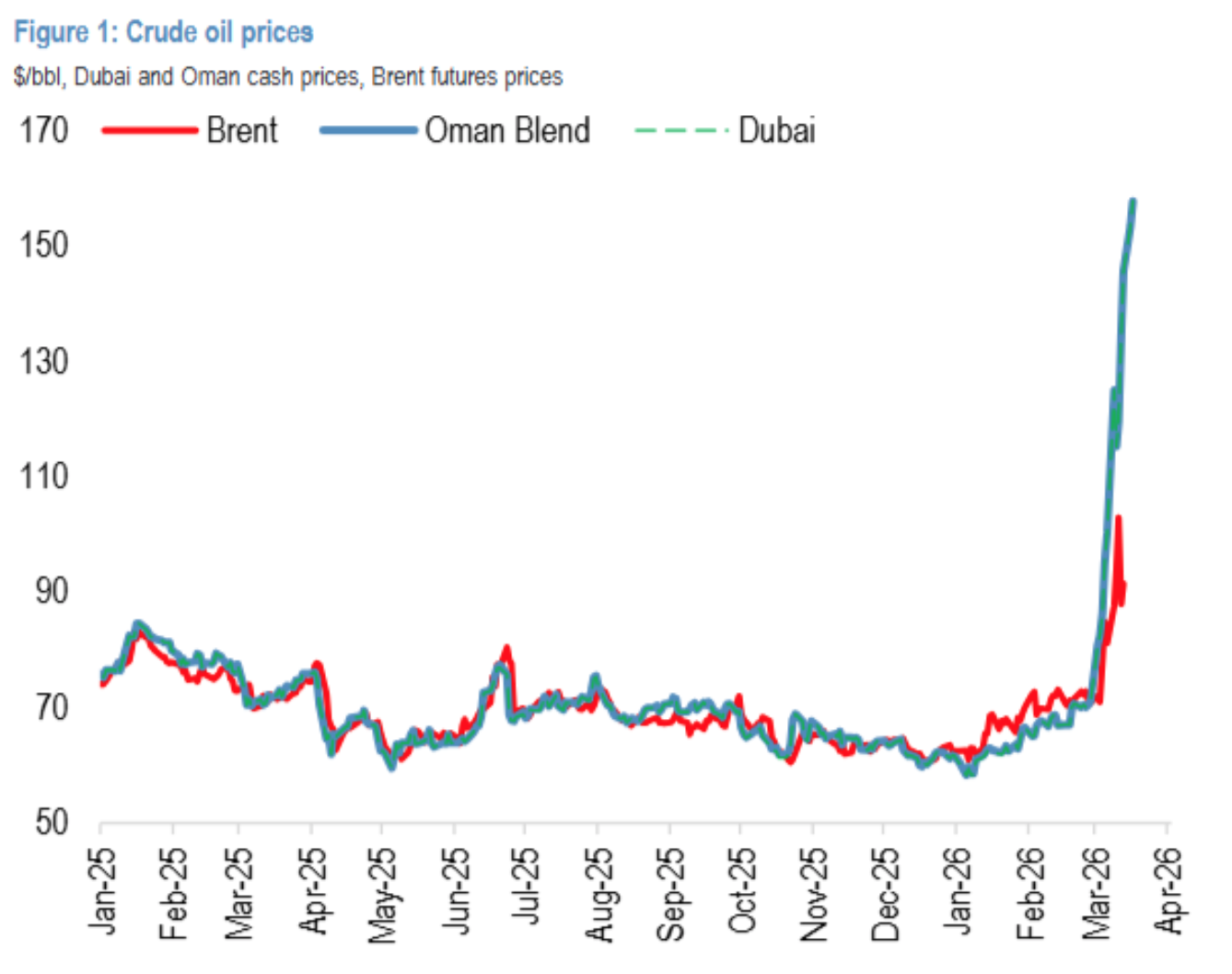

The global energy market is experiencing an unprecedented “dual-track split”: Brent/WTI crude futures hover around the $100 per barrel mark due to strategic reserve releases and speculative position adjustments, while the Dubai/Oman spot prices, which directly reflect Middle Eastern supply and demand, have surged above $155 per barrel, with the spread widening to a historic extreme of $55. This split essentially reflects a decoupling between “financial pricing” and “physical supply and demand.”

As a key energy security “ballast” and cost-effective alternative energy source, coal’s strategic value and commodity attributes are being systematically reassessed.

The global energy market is undergoing an unprecedented “dual-track split”: Brent/WTI crude futures fluctuate around $100 per barrel influenced by strategic reserve releases and speculative trading, while the Dubai/Oman spot prices, which directly mirror Middle Eastern supply and demand, have soared above $155 per barrel, with the spread reaching a historic extreme of $55. This split is fundamentally a decoupling of “financial valuation” from “physical supply and demand.”

In this context, coal, as a “ballast” for energy security and a highly cost-effective substitute, is being systematically reevaluated for its strategic and commodity value.

① Fundamental reversal: January-February 2026, domestic coal supply (production + imports) decreased by 0.1% year-on-year, while downstream demand (thermal power, chemicals, construction materials) increased by 3.1%, revealing a supply-demand gap. The entire industry chain (ports, power plants, coking plants) is moving toward inventory reduction.

③ Cognitive restructuring: Market perception of coal is shifting from “cyclical bulk commodity” to “defensive core asset with high cash flow, high barriers, and high dividends.”

While WTI futures traders on the NYMEX focus on the $93 per barrel level, spot buyers in the Persian Gulf face a very different market: Dubai crude spot prices have surged to $157.66 per barrel, with a total increase of 121.31% this month alone. The $55 spread results from regional inventory overhang, U.S. strategic reserve releases, and technical sell-offs in futures markets, but it does not reflect the true tightness of global physical supply.

The key variable is the blockage of the Strait of Hormuz. As the transit route for about one-third of global seaborne crude oil, current shipping is nearly halted. The only export route outside the Strait, the port of Fujairah in the UAE, has been repeatedly suspended. This means even countries like Saudi Arabia with idle capacity cannot deliver oil to Asian buyers at affordable costs. For countries like Japan, Korea, and Europe, which depend on Middle Eastern oil by 60-70%, “getting oil” is more urgent than “getting cheap oil.” Historical experience shows that whenever the oil price system experiences systemic disruption and spreads beyond substitution thresholds, coal will activate its substitution logic. Currently, the heat value ratio between crude oil and coal has deviated significantly from normal ranges.

For coastal power plants and coal chemical enterprises, the decision logic is clear:

① Direct combustion substitution: In some dual-fuel units, when oil prices exceed $100 per barrel, fuel oil power generation becomes uneconomical, prompting increased coal consumption to ensure power supply.

② Cost-driven: High crude oil prices directly raise diesel and fuel oil costs, which in turn increase costs for coal mining (mine machinery oil) and transportation (trucks, rail, shipping), supporting coal prices from the cost side.

③ Import substitution: The international coal market also faces resource mismatches. Suppliers in Indonesia and Australia, seeing the high prices of Middle Eastern oil, are strongly inclined to hold back and resist price declines. Although domestic import coal costs are currently high, leading to limited transactions, this “low volume decline” situation is unsustainable. Once port inventories reach critical levels, imported coal prices will quickly align with the energy premium implied by Dubai crude.

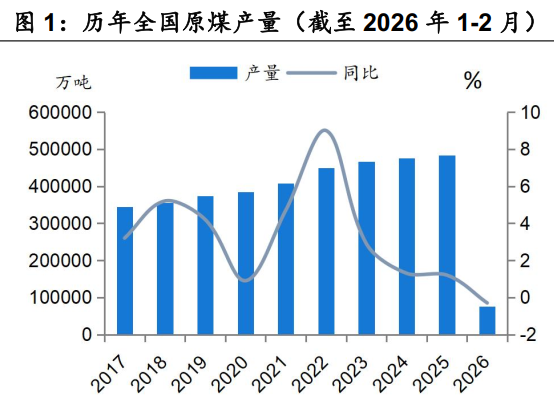

Data from the National Bureau of Statistics paints a clear picture of improving supply and demand dynamics.

① Supply side: Production contraction, limited import growth

Domestic production: January-February 2026, industrial raw coal output was 760 million tons, down 0.3% year-on-year. Although the decline narrowed compared to December 2025, the daily average output was 12.93 million tons, down 41,000 tons per day (4.1 million tons annualized). This confirms that under strengthened safety production constraints and normalized “inspection of excess production,” domestic supply elasticity has significantly diminished.

Coal imports: January-February imports totaled 77.22 million tons, up only 1.5% year-on-year, a sharp slowdown of 10.4 percentage points from December 2025. February, affected by the Spring Festival holiday and the narrowing price gap, saw a year-on-year decline. Coupled with soaring maritime shipping costs due to geopolitical conflicts, total coal imports in 2026 are unlikely to sustain the high growth of 2025, possibly even declining year-on-year.

Overall, the combined domestic supply (production + imports) in January-February decreased by 0.1% year-on-year, shifting from growth to decline.

② Demand side: Thermal power shifts from decline to growth; non-electric demand shows strong resilience

Contrary to widespread pessimism, demand data for January-February demonstrates strong resilience.

Thermal power: Industrial thermal power output increased by 3.3% year-on-year, reversing the 3.2% decline in December 2025, a strong turnaround of 6.5 percentage points. Amid slowing growth in wind, solar, and nuclear power, thermal power again plays a foundational role in energy security.

Non-electric demand:

Chemicals: Methanol weekly average production increased by 6.5% year-on-year, highlighting the economic advantage of coal chemical industry under high oil prices.

Construction materials: Cement output grew by 6.8% year-on-year, with infrastructure investment (+9.76%) beginning to show effects.

Coking coal: Production increased by 1.1% year-on-year.

Based on the downstream consumption proportions from the China Coal Industry Association (electric power 61%, chemicals 9%, construction materials 5%, steel 16%), the four major sectors collectively drove a 3.1% year-on-year increase in coal consumption in January-February, accelerating by 2.7 percentage points from December 2025.

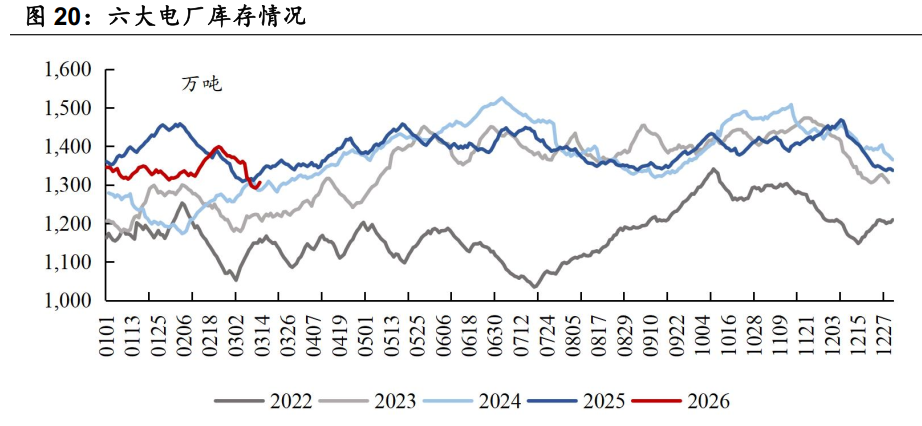

③ Inventory: Full destocking, price elasticity poised

The direct result of supply-demand gaps is a significant reduction in inventories.

Thermal coal: By the end of February, northern port inventories decreased by 3.921 million tons to 24.406 million tons, down 4.85 million tons year-on-year.

Coking coal: Inventories across production, ports, coking plants, and steel mills are all being destocked.

Currently, the available days of power plant inventories in eight coastal provinces remain relatively high, which is a primary factor suppressing short-term spot prices. However, high inventories are the result of active destocking, not weak demand. Once power plants judge that coal prices have limited downside or import coal arrivals are hindered, a concentrated replenishment cycle will quickly trigger price increases.

① Long-term supply constraints

Years of supply-side structural reforms have clarified the capacity ceiling of the coal industry. Unlike past cycles characterized by “release chaos” and “strict control,” under the hard constraints of “dual carbon” goals and safety production, even with high profits, capacity expansion is difficult to be disorderly. This implies a systemic upward shift in the price center and reduced volatility in the future.

② Reassessment of energy security premium

The turbulence in the Middle East is a Damocles sword hanging over major economies. As the world’s largest energy importer, China must ensure its energy supply “in its own hands.” Coal, as the most domestically controllable energy resource, is being elevated to an unprecedented strategic level. This strategic value will ultimately translate into long-term profitability and valuation premiums through pricing mechanisms.

③ Reshaping of high-dividend and state-owned enterprise value

In a low-interest-rate environment, coal companies characterized by “high profits, high cash flow, high dividends” are becoming scarce defensive assets. Since 2025, major state-owned enterprises like China Energy and China Coal Group have initiated increased holdings and asset injections into listed subsidiaries. This not only demonstrates confidence but also, under a new round of SOE reform, aims to improve the quality of listed companies and enhance shareholder returns. Asset injections will directly increase resource reserves and production scale, providing external growth potential.

Conclusion: The global energy market stands at a critical crossroads. The fire in the Strait of Hormuz has blown open the $55 gap between WTI futures and Dubai spot, awakening market awareness of “physical energy security.” For China, this split signifies an amplified risk exposure to oil import dependence, while coal, as a self-controlled foundational energy, has never been more strategically important.

The coal industry has entered a new stage of “rigid supply, resilient demand, and value reshaping.” Data from January-February 2026 clearly shows: the supply-demand gap is forming, inventories are being destocked, and the price bottom has been established.

Risk warning and disclaimer

Market risks exist; investments should be cautious. This article does not constitute personal investment advice and does not consider individual users’ specific investment goals, financial situations, or needs. Users should consider whether any opinions, views, or conclusions herein are suitable for their particular circumstances. Invest accordingly at their own risk.