Trade

Basic

Futures

Futures

Hundreds of contracts settled in USDT or BTC

Options

HOT

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Futures Kickoff

Get prepared for your futures trading

Futures Events

Participate in events to win generous rewards

Demo Trading

Use virtual funds to experience risk-free trading

Earn

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

NEW

Trade on-chain assets and enjoy airdrop rewards!

Futures Points

NEW

Earn futures points and claim airdrop rewards

Investment

Simple Earn

Earn interests with idle tokens

Auto-Invest

Auto-invest on a regular basis

Dual Investment

Buy low and sell high to take profits from price fluctuations

Soft Staking

Earn rewards with flexible staking

Crypto Loan

0 Fees

Pledge one crypto to borrow another

Lending Center

One-stop lending hub

VIP Wealth Hub

Customized wealth management empowers your assets growth

Private Wealth Management

Customized asset management to grow your digital assets

Quant Fund

Top asset management team helps you profit without hassle

Staking

Stake cryptos to earn in PoS products

Smart Leverage

NEW

No forced liquidation before maturity, worry-free leveraged gains

GUSD Minting

Use USDT/USDC to mint GUSD for treasury-level yields

More

Blockworks Co-founder’s 27 Predictions for 2026: Ethereum’s Rise, Bitcoin’s Fade, Solana’s “Hiding,” and a Major Shakeup in the Crypto Industry

1h ago

The three most powerful individuals in the history of crypto VC, even making Dragonfly partners feel inferior

14h ago

Trending Topics

View More11.15K Popularity

20.03K Popularity

13.65K Popularity

6.9K Popularity

94.69K Popularity

Hot Gate Fun

View More- MC:$0.1Holders:10.00%

- MC:$3.56KHolders:10.00%

- MC:$3.56KHolders:10.00%

- MC:$3.56KHolders:10.00%

- MC:$3.6KHolders:10.00%

Pin

Article 1 | Depth Analysis of Perp DEX: Hyperliquid, Aster, Lighter, edgeX

Hyperliquid

This generation of Perp DEX has fundamentally changed compared to the previous generation of Perp DEX like “GMX, DYDX”. Since it is still a Perp DEX at its core, the title will still discuss it as Perp DEX.

Starting with “Perp DEX”, it rapidly rose to prominence and became well-known.

Hyperliquid is an L1 public chain, just like Ethereum and Solana. Hyperliquid has a grand vision to create a blockchain that supports all finance and a high-performance on-chain financial trading infrastructure. Hyperliquid offers both perpetual contract trading and spot trading, and it is recently promoting the stablecoin USDH.

Its development path can be glimpsed from HIP, from HIP-1, HIP-2 to HIP-3, and recently the community has proposed HIP-4. HIP-4 aims to create “Event Markets” similar to Polymarket, further expanding the product boundaries of Hyperliquid. In simple terms, it is a binary market traded on HyperCore, which differs from traditional perps in that the events do not rely on continuous oracles or funding fees; the price is entirely determined by trading behavior. This proposal has also received Jeff's affirmation (the discussion about HIP will not be elaborated here, a dedicated research article will be written later).

Hyperliquid is also affectionately referred to by the community as “On-chain Binance”, a name that makes Binance executives a bit anxious. Alternatively, Hyperliquid can be called “AWS of Liquidity”, which sounds a bit sexier.

Hyperliquid L1 Technical Architecture and Performance

The Hyperliquid team has developed a high-performance Layer-1 blockchain specifically designed for trading, starting from “first principles” to address issues such as poor liquidity and trading experience, opaque black-box systems, and fraud in the crypto market. The architecture is divided into two parts: HyperCore and HyperEVM.

HyperCore is an on-chain matching engine responsible for the placing, matching, margin, and clearing of central limit order books (CLOB), with the entire process completed on-chain. Choosing CLOB over AMM is the right decision for Hyperliquid; the experience with the previous AMM Perp DEX was really poor. CLOB is also the common choice for the current mainstream Perp DEXs. (Aster, Lighter, and edgeX also use CLOB, among which Aster has both AMM and CLOB).

HyperEVM is a universal smart contract layer that shares consensus with HyperCore, maintaining compatibility with the Ethereum EVM, making it easier for other applications to integrate exchange states. The consensus adopts the improved HotStuff's HyperBFT (Proof of Stake), ensuring consistent transaction ordering across the network without relying on off-chain matching.

This tightly coupled sharding design brings speeds close to centralized exchanges: median transaction latency of about 0.2 seconds (99% of transactions < 0.9 seconds latency), peak throughput of up to 200,000 transactions per second (official HyperLiquid data). The block production and confirmation in Hyperliquid are very fast, achieving sub-second finality. Due to its fully on-chain order book and matching, it offers high transparency while still maintaining outstanding performance, truly achieving “CEX speed on-chain”. Currently, Hyperliquid has not explicitly adopted EigenLayer's AVS (Active Validation Service) scheme, mainly relying on its own chain and consensus to ensure performance and security, performance and security are directly provided by its own chain, without relying on ETH's re-staking network. As of September 2025, the number of active nodes in Hyperliquid L1 is 24.

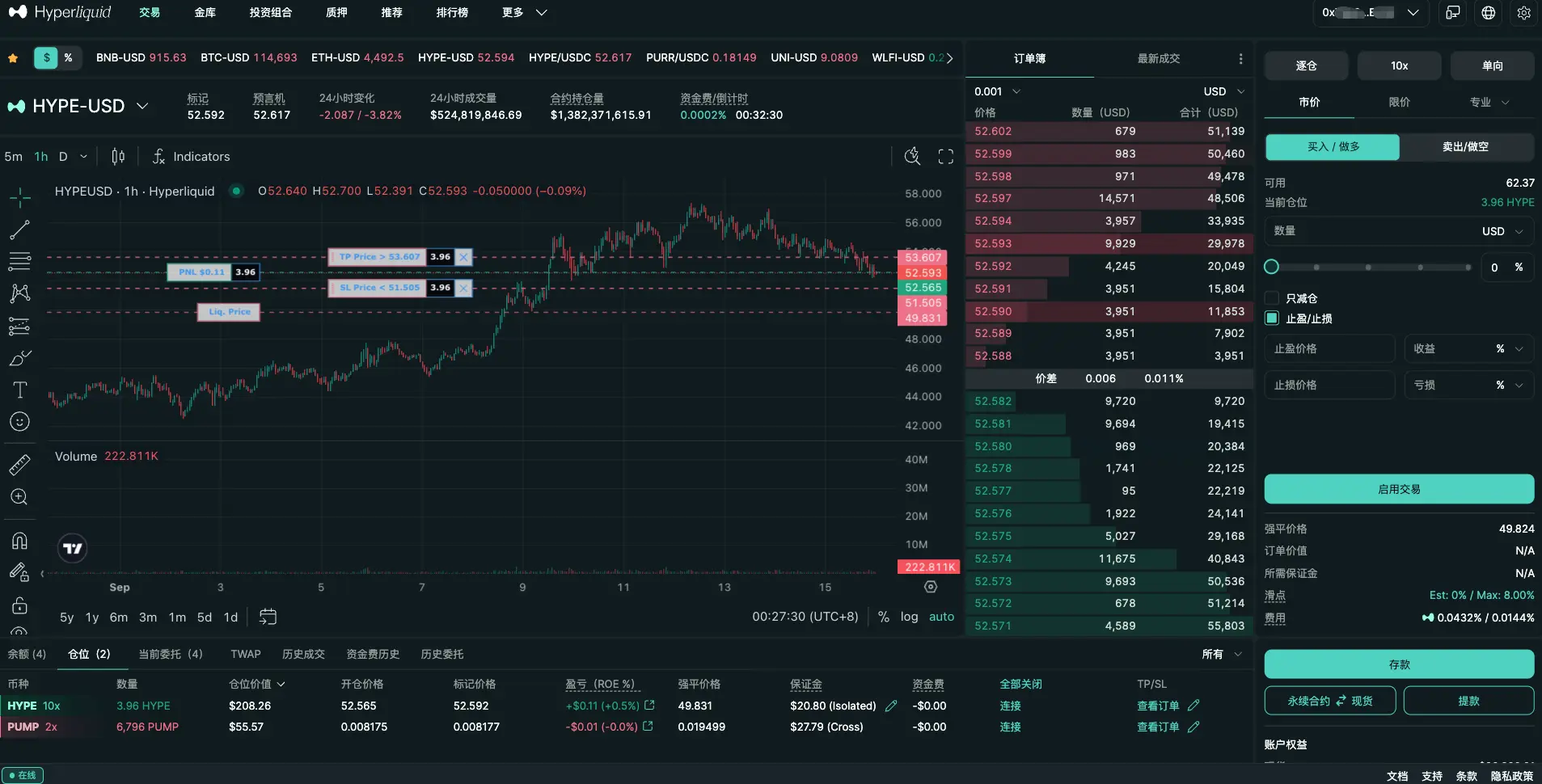

User Experience and Interface

Hyperliquid offers a trading experience consistent with leading CEXs. The user interface adopts a traditional order book + candlestick chart design, supporting advanced order types such as limit orders, take profit, and stop loss, along with professional trading tools. Trade settlement is almost instantaneous (sub-second level), and the interface operation feedback is smooth with no lag. It caters to the needs of both professional traders and ordinary retail investors. By the way, the sound prompt of “da” when opening or closing a position is quite pleasant.

Users can access permissionless + non-custodial trading via a web3 wallet, but they need to bridge assets to Hyperliquid L1 for use. Currently, USDC can only be deposited through the Arbitrum chain. An Agent wallet is then generated (which has only trading permissions, no transfer permissions, and the private key is stored locally), allowing for opening and closing positions without the need for further signatures, providing a smooth overall experience. Users are indifferent to this Agent wallet.

Hyperliquid is closely connected to the community and responds quickly. For example, after a brief downtime caused by an API failure in July 2025, the team quickly compensated users for approximately $2 million in losses, demonstrating a “quick response and accountability” approach. Users had a great experience, and the community praised it.

Liquidity and Trading Depth

As a leader, Hyperliquid possesses extremely deep liquidity and trading volume. Its daily trading volume often reaches tens of billions of dollars, with a single month’s perpetual trading volume in July 2025 hitting approximately $319 billion, which propelled the monthly total perpetual trading volume across the entire chain to a new high ( $487 billion), with Hyperliquid accounting for about 65%. In mid-2025, Hyperliquid's market share stabilized between 75-80%, far exceeding other competitors. In August 2025, the single month’s perpetual trading volume accounted for 13.85% of Binance contracts, the highest historical ratio. (The Block data)

The platform supports over a hundred trading pairs, covering mainstream coins and long-tail assets, with quick responses to listings. Due to the use of the on-chain order book model, users' order depth and matching are transparent and visible; coupled with the entry of professional market makers and the introduction of the HLP market-making pool, Hyperliquid achieves extremely low spreads and low slippage for large transactions on mainstream coins.

Its total locked value (TVL) is also far higher than its competitors: as of September 2025, the platform's TVL is approximately $2.7 billion. This large amount of capital and depth allows Hyperliquid's contract market to have trading depth and stable funding rates close to Binance in most cryptocurrencies.

The fee structure and incentive mechanism are similar to those of CEX. The basic trading fees for Hyperliquid are Maker 1.5bps, Taker 4.5bps, which are slightly lower than mainstream CEXs. Currently, users who stake HYPE tokens can also enjoy fee discounts, with a maximum discount of 40% (requires staking over 500,000 HYPE ), similar to Binance's holding of BNB and VIP level binding.

Vaults

The Hyperliquid treasury consists of three parts: AF, HLP, and user treasury.

Vault A: Assistance Fund (AF) AF is positioned as the protocol's “treasury”/buying engine. It is mainly used for repurchasing (often accompanied by burning) HYPE; simultaneously, it is used for user compensation during special events (such as the automatic compensation of approximately 2 million USDC after the API interruption on 2025-07-29). The assets of AF are primarily in HYPE, which reduces slippage and execution complexity during large transactions/compensations.

About 93% of the platform's transaction fees are injected into the fund for repurchasing and burning HYPE tokens, with another 7% allocated to the HLP liquidity pool. This design creates a positive feedback loop: increased trading volume → higher fee income → more tokens repurchased and burned (increasing token value) and benefits for the liquidity pool → attracting more users and liquidity.

Data source asxn

Protocol Vault B: HLP (Hyperliquidity Provider)

HLP positioning protocol-level market making + clearing backup (including Liquidator component). Anyone can deposit USDC to participate in HLP's PnL distribution, with the current annual interest rate of about 6.7%, and no management/performance fees (unlike user vaults). Deposits can be redeemed after 4 days. The HLP mechanism makes market-making liquidity “open and transparent in rules,” reducing reliance on private agreements with market makers in traditional markets.

User Vaults

Composed of a Vault Leader (manager, trading with their own strategy) and Depositor (investor, sharing PnL according to their contributions). Similar to a secondary fund and a CEX copy trading system. The Leader takes a 10% profit share (only when profitable), and the protocol treasury does not take a share.

Community Development and Team

Community Development: Hyperliquid has a highly active global community, with stronger presence in Europe and America compared to the Chinese-speaking regions. The official team is highly active on social media platforms like X (Twitter), maintaining a long-term market share at the top and creating network effects in the perp DEX sector.

The enthusiasm of community discussions is also reflected in the value of the tokens. Hyperliquid airdropped its genesis token HYPE in November 2024, distributing a total of 310 million tokens (accounting for 31% of the total supply) to early users. After the HYPE airdrop, the total market capitalization briefly reached tens of billions of dollars, providing substantial returns for early participants in the community and establishing a good reputation in the decentralized community. User growth mainly relied on word-of-mouth marketing and excellent products, rather than excessive marketing. This is somewhat similar to Tesla.

Team Background and Funding Status: Hyperliquid was founded by Jeff Yan, who previously worked at the traditional finance high-frequency trading company Hudson River Trading and has a background from Harvard University. The core team consists of only about 11 people, known for their elite small group and rapid iteration. According to Jeff, the project has been entirely self-funded since its inception, rejecting venture capital investment to ensure independent decision-making and prioritize user interests. This approach of “no VC, no reserved private placements” has enhanced community trust and allowed the team to focus more on technology and the product itself. Most team members come from prestigious universities and top technology and financial institutions, and reports indicate that they have attracted some traditional finance executives to join the advisory team (including former CEOs of large banks taking board positions). However, market rumors suggest that Hyperliquid may have raised funds through associated public entities, indicating strong financial capabilities (the platform's treasury holds over $500 million in reserves). Overall, the Hyperliquid team is low-key and pragmatic, leveraging their deep technical and trading backgrounds to elevate the project to industry leadership within two years. This background also explains their extreme pursuit of product refinement and user experience.

The Essential Reasons for Rapid Growth

There are many discussions about the reasons for Hyperliquid's success. In addition to the well-structured team, excellent product technology, and user experience mentioned above, we can discuss from the perspectives of “Dao” and “Shu”, dividing it into different stages, and see what Hyperliquid did right.

First, from the perspective of “technique”.

Phase One: Airdrop Incentives

Before HYPE TGE, there were expectations for airdrops, and most users came to gain points and airdrops by increasing trading volume. At that time, Hyperliquid did not receive much attention from mainstream CEXs and was not seen as a competitor. Everyone believed that Hyperliquid would fade into obscurity like GMX and DYDX after the TGE, with no one trading it.

Phase Two: Compliance Regulatory Dividends

After the HYPE TGE, Hyperliquid's trading volume not only did not decrease but actually increased. People began to realize that something was off, and the general consensus is that the crypto market is under pressure from regulatory compliance, making it difficult for mainstream CEXs to operate in the European and American markets, such as Binance. This part of the “lost” users has been absorbed by Hyperliquid (which can be seen from the distribution of user visits on the Hyperliquid website). Additionally, some users who found KYC to be a bit “inconvenient” also found a suitable tool.

At this point, Hyperliquid has been regarded as a competitor by Binance, OKX, Bitget, etc., and has taken some “action” to target Hyperliquid. (Traces can be found in the community, but will not be elaborated here)

Stage Three: Build Codes - Channel Distribution is King

KOL rebates & Affiliate are common user acquisition strategies for CEX. In addition to branding, PR, community, SEO, campaigns, etc., BD-oriented KOL rebates are essential growth paths and very important.

Different CEXs have varying proportions of users brought in by KOL commissions. For instance, Binance might be around 50%, while Bitget could be about 70%. Additionally, the smaller the CEX, the higher the KOL commission rate, resulting in a greater proportion of users and trading volume. In fact, many small CEXs offer commission rates of 90%-100%, utilizing a “eating customer losses - subsidizing commissions” “flywheel” for growth.

The rebate rate for Hyperliquid is only 10%, and it is limited to the first 1 billion in trading volume. Based on an average fee rate of 3 bps, if the person you invited contributed 300K in fees, you would only earn 30K in income. The focus of Hyperliquid is not on rebate invitations, but rather on Build Codes.

Few people realize the true power of Build Codes; it is a distribution strategy with genuine exponential potential. For developers, there is no longer a need to build high-performance order books or attract liquidity, as Hyperliquid provides the necessary infrastructure. For Hyperliquid, there is no longer a need to manage product promotion, user acquisition, or even product innovation, as all of this is entrusted to the builders' network. It's somewhat similar to a Swiss team I was part of before (with a UBS background) that created a Perp DEX using a white label solution; the direction was right, but the product strength was lacking. In fact, the previous Binance Broker and OKX's cloud exchanges/nodes were similar solutions; the essential difference of Build Codes is ease of access, low barriers to entry, and on-chain transparency.

Currently, Phantom wallet, Axiom, UXUY, PVP.trade, and others have integrated this solution. So far, Phantom has contributed approximately 40K new users, and PVP.trade has generated an income of 7.5m in a single day. At present, I have also completed the development of a basic version of a perp DEX and am ready to leverage previous experience and channel resources for growth. Those who are interested can communicate together.

In addition to Build Codes, there are also the powerful tools CoreWriter and HIP-3, but the threshold is slightly higher. Due to space constraints, I won't elaborate here.

“Tao” - Those who attain the Tao will receive much assistance

Although the analysis of the reasons for Hyperliquid's success above is relatively detailed, it is not essential. Many interpretations of Hyperliquid's success also remain superficial.

But the essence can be summarized in one sentence: Hyperliquid has taken up the banner of “blockchain spirit”—openness, transparency, decentralization, and user sovereignty. Just as Binance once carried this banner to challenge traditional finance, BTC maximalists, industry OGs, and regular crypto users all stand by Binance. What truly brings people together is the genuine blockchain spirit.

From the user's perspective, many CEXs indeed have issues such as centralized black boxes, taking customer losses, and competing against users. From the perspective of CEX owners, they also face increasingly strict compliance and regulatory challenges. Therefore, many CEXs are turning to DEXs.

So, Binance's heir - Aster has emerged. For details, see the next article: “In-depth Analysis of Perp DEX: HperLiquid, Aster, Lighter, edgeX (2)”

(The above is just a personal opinion and not investment advice. Please feel free to point out any errors.)