Solana Digital Asset Fund Company Forward Industries announced on Thursday that it repurchased over 6 million shares from institutional investors, reducing outstanding common stock by approximately 7.4%. The transaction was financed through a $40 million cryptocurrency-backed loan provided by Galaxy Digital. At the same time, the company’s SOL holdings also face an unrealized loss of over $1.1 billion on paper.

Repurchase Financing Mechanism and Strategic Logic

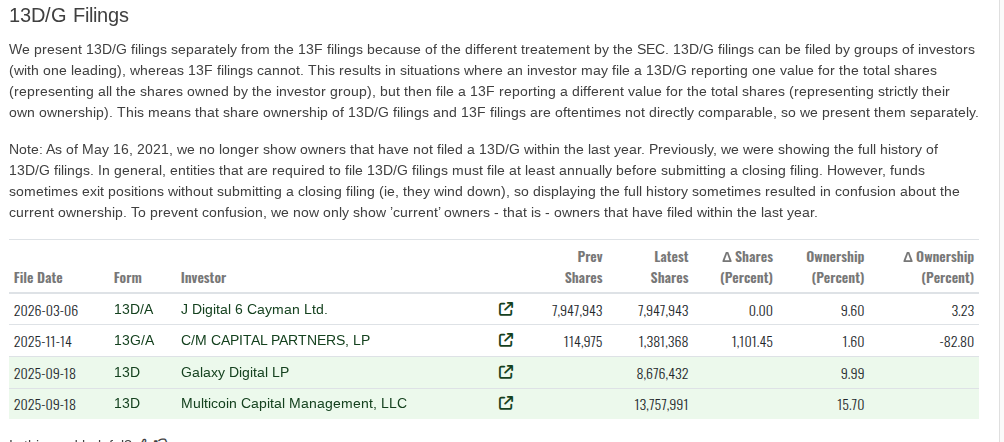

(Source: Fintel)

(Source: Fintel)

This repurchase is part of Forward Industries’ $1 billion stock buyback plan approved by the board in November last year.

Chief Investment Officer Ryan Navi explained the core logic of this operation to the media: “If the stock trading price is significantly below our net asset value (NAV), then continuing to buy back our own shares makes more sense than buying SOL on the open market, because buying back shares effectively allows us to purchase more SOL at a discount.”

This approach aligns closely with the strategies of other digital asset fund companies. For example, Ethereum asset fund company SharpLink explicitly states that it will only buy ETH when the company’s market value/NAV exceeds 1; otherwise, it prioritizes share repurchases, which indirectly increases crypto holdings at a lower cost.

Galaxy Digital’s $40 million loan is secured by staked SOL in Forward’s treasury. This financing method, using crypto assets as collateral to buy back shares, means the company can obtain USD liquidity without selling SOL, while simultaneously executing a “buy more SOL at a discount” operation at the stock level.

Forward Industries’ Solana Holdings and On-Paper Loss Status

Forward Industries entered the market relatively aggressively last fall, investing about $1.58 billion to acquire approximately 6.8 million SOL at an average cost of around $232 per share. However, as the overall crypto market declined, SOL’s price fell to $88.86, resulting in an unrealized paper loss of over $1.1 billion. According to blockchain analytics firm Artemis, among all digital asset fund companies, Forward ranks sixth in terms of paper loss.

Current holdings overview:

- SOL holdings: Over 7 million (including rewards from staking)

- SOL market value: approximately $614 million (based on current market price)

- Unrealized paper loss: over $1.1 billion

- FWDI stock: closed Thursday at $4.95, down over 83% in the past six months, 89% below the September high of $46.00

In addition to stock buybacks, Forward is actively controlling costs, with operational expenses expected to decrease by up to 45% in Q1, demonstrating efforts to enhance net value per SOL through both revenue and expense management.

Frequently Asked Questions

Is there a risk in Forward Industries’ debt-backed stock repurchase?

The core risk of using SOL as collateral for loans is that if SOL’s price further declines, the collateral’s market value may fall below the liquidation threshold, forcing the company to add collateral or repay early. With SOL’s price dropping from an average purchase cost of $232 to about $89 (a decline of over 60%), leveraging to repurchase shares is a high-risk strategy that requires precise management. It also strongly reflects management’s confidence in SOL’s long-term value.

Why is “buying back stock equivalent to buying SOL at a discount”?

Forward’s logic is that the market price of FWDI shares reflects the market’s valuation of the company’s “SOL net value per share.” If the stock price is below the actual value of the company’s SOL holdings per share (i.e., at a discount), then each dollar spent on buybacks effectively acquires more SOL than directly purchasing SOL on the open market. This arbitrage makes share repurchases at a deep discount more efficient than directly increasing SOL holdings, assuming the company believes in SOL’s long-term appreciation.

Does the $1.1 billion paper loss mean Forward Industries faces bankruptcy risk?

Paper losses reflect that the market value of holdings is below cost and do not directly equate to cash flow losses or imminent bankruptcy. Forward owns over 7 million SOL, with a market value of $614 million, and there is no immediate forced liquidation requirement. The real risk would arise if the company’s debt (including Galaxy Digital’s $40 million loan) triggers a margin call or if operational cash flows cannot support daily expenses, potentially leading to more serious financial issues. Navi stated that the company is actively reducing operating expenses to mitigate this potential pressure.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.