Against the backdrop of the continued evolution of the DeFi “Curve Wars,” the role of CVX has gone far beyond that of an ordinary reward token. It connects veCRV voting power, protocol revenue distribution, Gauge incentive competition, and governance decision-making structures, gradually making it one of the most important governance assets in the Curve ecosystem.

As Convex continues expanding into veToken ecosystems such as Frax, FX Protocol, and Prisma, the governance scope and yield structure of CVX have also evolved from a single Curve yield optimization tool into a more complex DeFi incentive coordination layer.

The Protocol Positioning of the CVX Token

CVX is mainly used for protocol governance, yield incentives, and veCRV rights coordination. Convex itself does not directly replace Curve. Instead, it acts as a yield optimization layer within the Curve ecosystem, improving the capital efficiency of liquidity funds by aggregating veCRV.

Under the traditional Curve mechanism, users who want higher yields usually need to lock CRV for the long term to obtain veCRV and participate in complex governance and Boost management processes. Convex, however, aggregates veCRV in a unified way, allowing ordinary users to indirectly access higher yields without locking large amounts of CRV themselves.

Within this system, the role of CVX is essentially to connect “protocol governance” with “yield incentives”. It represents not only governance rights within Convex, but also Convex’s influence over veCRV incentive distribution in the Curve Wars. As a result, the value of CVX is closely linked to the amount of veCRV controlled by Convex, Curve yield flow, and the protocol’s governance influence.

From an industry positioning perspective, CVX is usually seen as a typical DeFi governance token. In reality, however, the structure behind it is closer to a composite asset that combines “yield rights + governance rights + incentive coordination rights.”

What Role Does CVX Play in Convex Finance?

One of the most important roles of CVX is participation in Convex’s governance system. Users can obtain voting power by locking CVX and participate in Gauge weight allocation, protocol parameter adjustments, and governance over certain yield mechanisms. Because Convex aggregates a large amount of veCRV, CVX governance outcomes can also indirectly affect the flow of incentives within the Curve ecosystem.

In addition to governance, CVX also plays a role in yield distribution. CVX holders can stake their tokens to receive a portion of platform revenue, including reward assets from ecosystems such as Curve and Frax. These rewards are usually first converted into cvxCRV or other representative assets before being distributed to CVX stakers.

CVX is also the core reward asset in Convex’s incentive system. When Curve LP users earn CRV through Convex, the protocol distributes additional CVX based on the scale of those CRV rewards. This structure effectively creates a “two-layer incentive model,” where users receive both native Curve yields and additional Convex incentives.

As Convex expands into other veToken ecosystems such as FX Protocol and Prisma, the role of CVX is gradually extending from a Curve-specific governance asset into a cross-protocol incentive coordination tool.

CVX Issuance Mechanism and Supply Structure Explained

The maximum supply of CVX is set at 100 million tokens, and its issuance structure is directly tied to CRV earnings on the Convex platform. Unlike many tokens that are fully released all at once, CVX uses a dynamic release mechanism. When users earn CRV through Convex, the system mints new CVX proportionally.

This “minting based on yield” structure directly links CVX growth to Convex platform activity, the scale of Curve yields, and LP usage. When the scale of Curve yields on Convex increases, the distribution speed of CVX usually rises as well.

However, the CVX minting ratio is not fixed forever. The protocol uses a “Cliff Reduction” mechanism, meaning that after a certain amount of CVX is released, the ratio for newly minted CVX gradually decreases. As supply approaches the maximum cap, the rate of new CVX issuance therefore slows down over time.

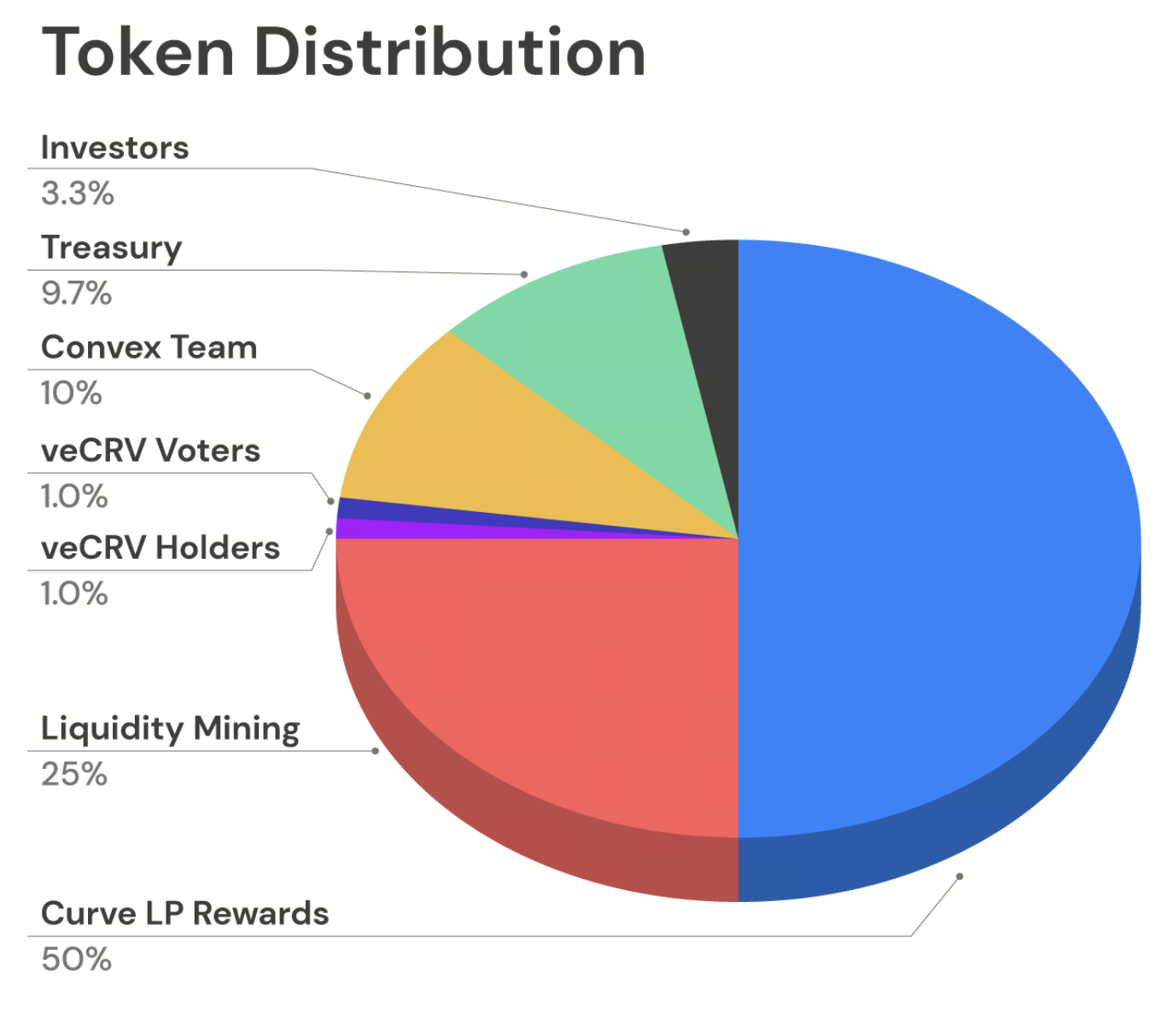

In the initial allocation structure, roughly half of CVX was used for Curve LP incentives, while the rest was allocated to liquidity mining, the team, investors, the treasury, and a veCRV community airdrop. This structure reflects Convex’s strong early dependence on Curve ecosystem expansion and veCRV aggregation.

Source: convexfinance.com

The Relationship Between CVX, veCRV, and cvxCRV

CVX, veCRV, and cvxCRV are closely connected. veCRV is Curve’s governance lockup asset, while cvxCRV is the “tokenized veCRV” representative asset generated after Convex locks CRV.

When users deposit CRV into Convex, the protocol permanently locks those CRV and converts them into veCRV under unified management. Users then receive cvxCRV at a 1:1 ratio. In this way, ordinary users can indirectly access veCRV earning capacity without locking CRV for the long term themselves.

CVX sits at a higher layer of this structure. Through the governance mechanism, CVX holders can influence how Convex uses its aggregated veCRV, including Gauge voting direction and yield incentive allocation. In this sense, CVX essentially represents the “control-right governance layer” over Convex’s veCRV.

This structure allows Convex to build a multi-layer yield system around veTokens: the base layer is Curve’s veCRV, the middle layer is Convex’s cvxCRV, and the upper layer is CVX, which handles governance and incentive coordination.

Convex Finance’s Governance Mechanism

Convex governance mainly revolves around the Vote Locking mechanism. Users who want to participate in governance need to lock CVX for at least 16 weeks, and locked CVX receives corresponding voting power. This structure is somewhat similar to Curve’s veCRV model and is essentially a form of “time-weighted governance.”

Locked CVX not only allows users to participate in governance, but may also provide additional yield distribution. Because Convex redistributes part of its platform revenue to locked users, Vote Locking also functions as a yield incentive mechanism.

Convex governance usually focuses on how veCRV is used, Gauge voting weights, and protocol upgrade proposals. Since Convex aggregates a large amount of veCRV, its governance outcomes can effectively influence the direction of liquidity incentives within the Curve ecosystem.

To prevent long-idle locked positions from reducing governance efficiency, Convex also has a “Kick” mechanism. If users do not withdraw their assets for a long time after unlocking, other users can trigger a cleanup process and receive a small reward. In essence, this mechanism manages governance activity at the protocol level.

The CVX Incentive Model and DeFi Yield Distribution Logic

The CVX incentive model is built on top of Curve’s yield structure. Convex does not “create yield out of thin air.” Its core logic is to aggregate veCRV, improve the yield efficiency of Curve LPs, and then redistribute part of the yield to CVX holders.

When users provide Curve LP liquidity through Convex, they typically receive CRV rewards. The protocol then distributes additional CVX proportionally based on the scale of those CRV rewards. This means CVX distribution is tightly linked to Curve liquidity activity.

At the same time, CVX stakers can also receive a portion of platform fee revenue. These earnings may come from reward assets across different ecosystems, including Curve, Frax, and FX Protocol, and are distributed in forms such as cvxCRV and cvxFXS.

This structure effectively creates a typical DeFi “yield loop model”: Curve provides the base yield, Convex aggregates veCRV to improve yield efficiency, and CVX handles governance and incentive redistribution. As more veToken protocols connect to Convex, this yield coordination structure is gradually expanding across protocols.

How CVX Differs from DeFi Governance Tokens Such as CRV

One of the biggest differences between CVX and traditional DeFi governance tokens is that its value does not come only from protocol governance. It is deeply tied to veCRV aggregation capacity. CRV is Curve’s native governance asset, while CVX is more like a “second-layer governance asset” built around Curve’s incentive system.

Compared with ordinary governance tokens that are mainly used for proposal voting, CVX places more emphasis on controlling yield flows and incentive structures. Because Convex aggregates a large amount of veCRV, CVX governance outcomes can directly influence Gauge incentive competition within the Curve ecosystem.

In addition, CVX has a more complex yield model. Many governance tokens rely mainly on revenue from a single protocol, while CVX connects multiple veToken ecosystems, including Curve, Frax, and FX Protocol, giving it more diversified incentive sources.

From an industry perspective, CRV is closer to a base-layer protocol governance asset, while CVX is more like a “governance aggregation layer asset” built on top of veCRV. This is also one of the key reasons Convex was able to rise quickly during the Curve Wars.

Conclusion

CVX is the core governance and incentive token of Convex Finance. Its essential role is to coordinate veCRV aggregation, yield distribution, and the Curve incentive structure. Through Vote Locking, yield redistribution, and Gauge governance mechanisms, CVX has gradually become one of the most important governance assets in the Curve Wars.

Compared with traditional DeFi governance tokens, CVX places greater emphasis on “governance power aggregation” and “yield coordination capacity.” It not only connects to Curve’s veCRV system, but has also gradually expanded into other veToken ecosystems such as Frax and FX Protocol. As DeFi incentive models continue to evolve, the “governance aggregation layer” structure represented by CVX has also become one of the most representative examples of the veToken economic model.

FAQs

What Is CVX?

CVX is the native governance token of Convex Finance. It is used for protocol governance, yield distribution, and veCRV incentive coordination.

How Is CVX Different from CRV?

CRV is the native governance token of Curve Finance, while CVX is a governance aggregation asset built on top of Curve’s incentive system. It mainly handles veCRV aggregation and yield coordination.

What Is cvxCRV?

cvxCRV is the representative asset users receive after depositing CRV into Convex. It represents the user’s rights within Convex’s aggregated veCRV yield structure.

Why Do Users Need to Lock CVX?

Users need to lock CVX to participate in Convex governance and receive a portion of protocol revenue distribution.

What Is the Maximum Supply of CVX?

The maximum supply of CVX is 100 million tokens, and new issuance gradually slows as the release process progresses.