Unlike traditional financial services companies, Moody’s does not sell capital. It sells credit information and the ability to assess risk. Credit ratings help capital markets evaluate borrowers’ default risk, while analytics and data services help institutional clients manage risk, meet regulatory requirements, and improve decision making efficiency.

Because the credit rating industry has high market barriers, and financial data services often generate subscription based revenue, Moody’s has gradually built a business model with both high profit margins and stable cash flow. This is one reason MCO has long been viewed as an important global financial infrastructure company.

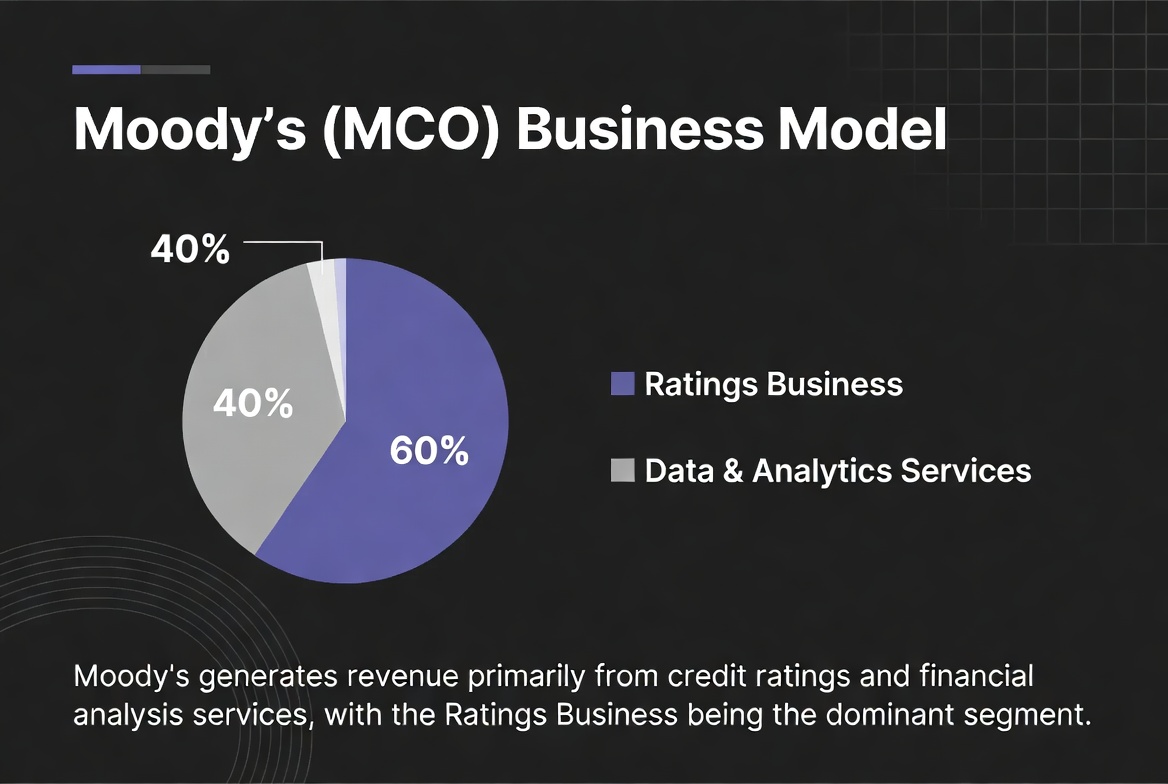

MCO is the stock ticker for Moody’s Corporation, which is listed on the New York Stock Exchange. Moody’s is an important participant in the global credit rating industry, with businesses spanning credit ratings, risk analytics, financial data, regulatory technology, and enterprise risk management solutions. Today, Moody’s is mainly made up of two business segments:

| Business Segment |

Main Function |

| Moody’s Investors Service (MIS) |

Credit ratings |

| Moody’s Analytics (MA) |

Risk analytics and data services |

The credit ratings business has long been the company’s core revenue source, while analytics and software have gradually become important growth drivers. By industry classification, Moody’s is usually considered a financial information services company rather than a traditional bank or insurer.

What Are Moody’s Revenue Sources?

Moody’s revenue mainly comes from two segments. The first is the credit ratings business. When companies issue bonds, financial institutions raise funds, or governments issue sovereign debt, they usually need to obtain a credit rating. Rating service fees are one of Moody’s most important sources of revenue.

The second source is the analytics and data services business. As financial markets continue to demand more data and stronger risk management, Moody’s provides clients with software platforms, financial data, credit research tools, and regulatory compliance solutions.

Overall, Moody’s revenue structure has gradually shifted from relying on a single ratings business to a model where ratings and data businesses operate side by side. This diversified revenue base reduces the company’s dependence on any single market cycle.

How the Credit Ratings Business Generates Revenue

The credit ratings business is Moody’s most representative business. When a company or government plans to issue bonds, it usually hires a rating agency to conduct a credit assessment. The rating agency analyzes the issuer’s financial condition, industry environment, cash flow capacity, and debt structure before assigning a credit rating.

After the issuer pays the rating fee, Moody’s prepares the rating report and continues to monitor the issuer over time.

Revenue from the credit ratings business is usually closely tied to bond issuance activity.

When bond markets are active and financing demand rises, demand for ratings typically grows as well.

When interest rates rise or capital market financing slows, ratings revenue may come under pressure.

For this reason, bond issuance volume is often seen as one of the important factors affecting Moody’s ratings business.

How Risk Analytics and Data Services Drive Growth

Risk analytics and data services have become one of Moody’s fastest growing business segments in recent years. Moody’s Analytics mainly serves:

-

Banks

-

Insurance companies

-

Asset managers

-

Corporate clients

-

Government departments

Its related products include:

As financial regulation continues to strengthen around the world, institutions have a growing need for risk management systems and data analytics tools. Compared with one time ratings projects, analytics services are usually based on long term contracts and subscription fees, which can create a more stable revenue stream. This is also an important reason Moody’s has continued to increase its investment in the analytics business in recent years.

Why Recurring Revenue Improves Business Stability

Recurring revenue is an important feature of Moody’s business model. Although the ratings business has high margins, it is more exposed to bond issuance cycles.

When market financing activity declines, the number of new ratings projects may fall.

The analytics and software business has a very different profile. Many financial institutions subscribe to Moody’s data platforms and risk management tools over long periods and continue paying service fees.

This model gives Moody’s more stable and predictable cash flow. From a business model perspective, a higher share of recurring revenue usually means:

| Feature |

Impact on the Company |

| Higher revenue stability |

Reduces market cycle volatility |

| Stronger customer stickiness |

Improves renewal rates |

| More predictable cash flow |

Supports long term investment |

| Greater valuation flexibility |

Strengthens market recognition |

Therefore, the development of analytics and data services not only drives revenue growth, but also improves the overall quality of Moody’s business model.

How the Financial Regulatory Environment Affects Moody’s Business

The financial regulatory environment is closely connected to Moody’s business. Credit ratings have long played an important role in bank capital regulation, insurance regulation, and bond market rules.

Regulatory frameworks in many countries and regions refer to credit assessments from rating agencies, making the rating system an important part of global financial infrastructure. At the same time, rating agencies themselves are also subject to strict regulation. Regulators usually require rating agencies to maintain transparent rating processes, independent analytical systems, and sound mechanisms for managing conflicts of interest.

After the financial crisis, major global markets further strengthened regulatory requirements for the rating industry. For Moody’s, higher regulatory standards increase compliance costs, but they also raise barriers to entry. This helps large rating agencies maintain long term competitive advantages.

How to Buy MCO (Moody’s) Stock

MCO is listed on the New York Stock Exchange and is one of the most representative publicly traded companies in the global credit rating industry. Investors can buy MCO shares through traditional securities brokers and participate in the potential rewards and risks tied to the company’s operating performance and financial market development.

In addition to traditional securities markets, some digital asset trading platforms also offer CFD products linked to US stock prices. For example, the Gate CFD market supports certain US stock related contracts for difference, allowing users to use digital assets to trade price movements. CFDs are leveraged derivatives, and their risk characteristics differ from those of actual shares. Before participating in trading, users should fully understand the product mechanism, margin requirements, and potential risks.

Conclusion

Moody’s (MCO) business model is built on two core businesses: credit ratings and risk analytics. The credit ratings business generates revenue from the global bond market, while the analytics and data services business provides ongoing growth momentum through a subscription model. As financial institutions increasingly need risk management, data analytics, and regulatory compliance support, the importance of the analytics business continues to rise. The industry barriers created by the ratings business, together with the recurring revenue generated by data services, form the core competitive strength of Moody’s business model.

FAQs

How Does Moody’s Mainly Make Money?

Moody’s mainly earns revenue through credit rating services and risk analytics services. The credit ratings business serves bond issuers, while the analytics business provides financial institutions with data, software, and risk management tools.

Why Does the Credit Ratings Business Have High Profit Margins?

The credit ratings business mainly depends on professional analytical capability and brand credibility, while its marginal costs are relatively low. At the same time, the industry has high barriers to entry, allowing it to maintain strong profitability.

What Is Moody’s Analytics?

Moody’s Analytics is Moody’s analytics and data services division. It mainly provides risk management software, financial data platforms, regulatory technology, and credit analysis tools.

Why Is Recurring Revenue Important to Moody’s?

Recurring revenue helps reduce the impact of bond issuance cycles on the company’s performance, while improving cash flow stability and customer retention.

Does Financial Regulation Affect Moody’s Business?

Financial regulation affects the rules of the ratings industry and also increases market demand for risk management tools, so it has an important impact on Moody’s business.

Is MCO a Financial Company or a Technology Company?

MCO is usually classified as a financial information services company. Its business combines credit ratings, financial data, analytics software, risk management services, and several related fields.